Opened an account with E.Sun in the end (they charge NT$200 per incoming transfer). But still not sure if there are better options available or not.

@qwert_zuiop Exchange rates as expected as you stated before? How do you get the better rate though?

200 TWD would be okay, when sending few thousands of € over here.`

Just do the exchange via the online banking. Then the rate should be less than 0.1NT$ from the exchange rate quoted from Bloomberg

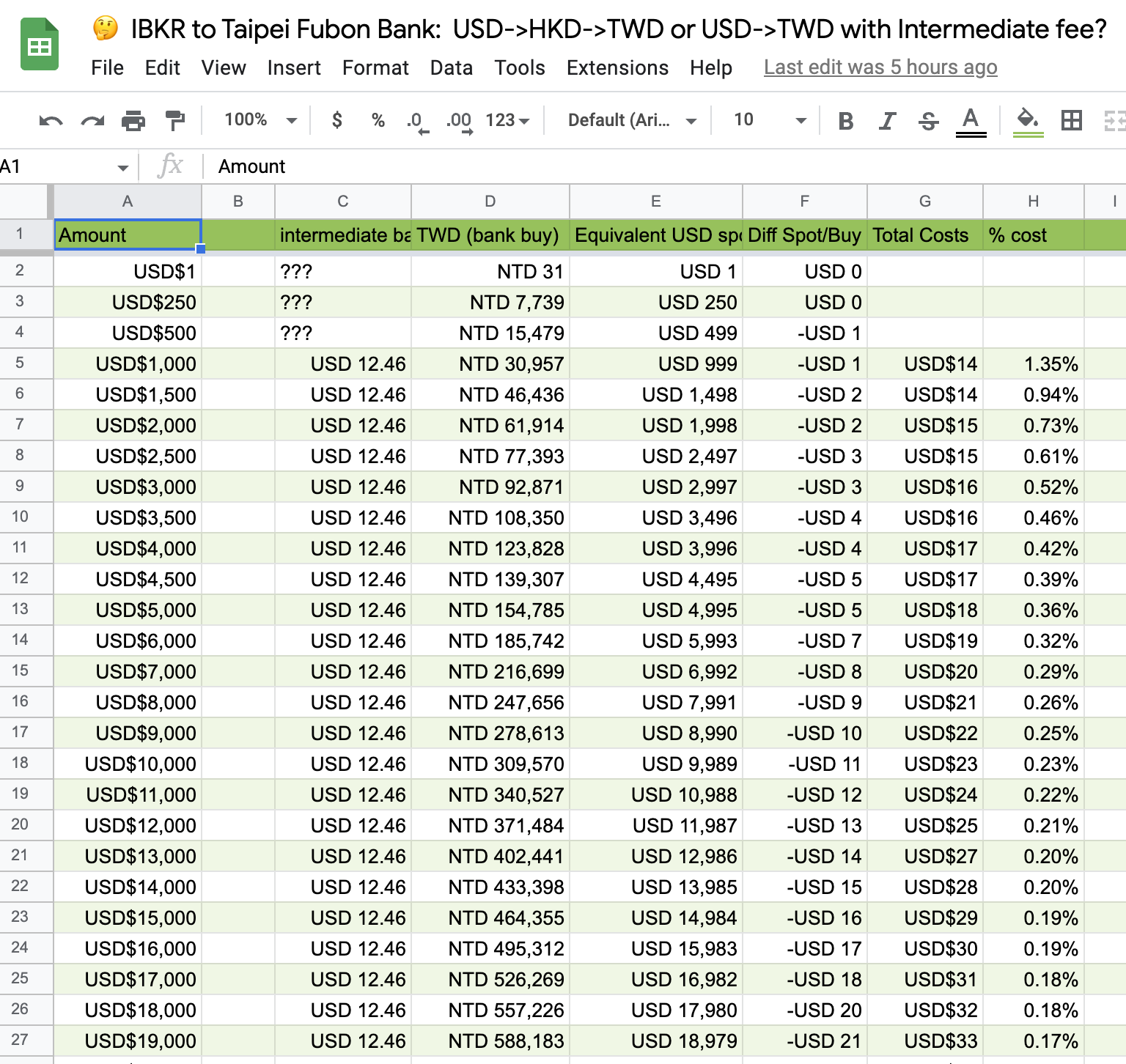

Trying to figure the “optimal” way to send USD from Interactive Broker to Taipei Fubon Bank.

A friend shared with me that the best way to go to not get hit by the intermediate bank fee is to convert USD to HKD in IBKR first (0.002% fee, it’s insignificant), and send it to a Taiwanese bank (without intermediate fee). IBKR has 1 withdrawal per month.

It seems that buy price for USD->TWD are better than HKD->TWD, so I’ve made this spreadsheet to know at what amount you shouldn’t be bothered and take the “hit”. The missing element is the intermediate fee. Anyone did it in the past and would know the answer?

The big question mark is the the intermediate bank fee, that could be anything between 0 and $100. Also I don’t know if banks take any additional conversion fee other than their buy price (probably?).

IBKR uses this intermediate bank to send to Fubon:

BANK OF AMERICA, N.A. SAN FRANCISCO, California, United States, BOFAUS6SXXX

US$ 100 would be quite unlucky, I would assume. In practice, it should be more between 0-25 US$.

I would be more worried about the fluctuations in the exchange rate between HKD / USD / TWD while the transfer is in progress.

In the end, you’ll probably have to try and see - and avoiding all fees will probably not be possible unfortunately…

When a swift wire is sent there’s a MT103 receipt. On it there’s a code for 71A. If it’s OUR then the taiwan bank won’t charge an incoming fee. You can ask for MT103 from some banks after they send the wire. MT103 - A standardised SWIFT payment confirmation

If you can find a bank that doesn’t use an intermediary, you can control the fees on both sides

For example when I send from chase US (premier), they don’t use an intermediary and cover both sender and receiver fees, so ESun doesn’t charge any receiving fees and neither does Chase (JP Morgan).

With some banks you can choose to cover receiver fees. With Citi US (they also don’t use an intermediary) I can choose to pay a fixed $15 to cover receiver wire fees, which is sometimes cheaper than ESun’s 200-1600NT receiving fees.

Maybe you can find out what intermediary banks your home country uses and then send a wire through them directly. In the US some big ones are Chase JP Morgan, Citi, Wells Fargo(?)

I did wire a few thousands USD on Friday afternoon in IBKR. It arrived on Monday morning. The intermediate bank (Band Of America SF) took USD 12.5. IBKR and Fubon didn’t take anything. Assuming it will remain the same amount matter how much, I think it does worth it over a few thousands.

Updated the spreadsheet. (Could be a good idea to try to gather all this data to have a more comprehensive path available to us )

anyways to my knowledge the only bank here without incoming SWIFT transfers fee is HSBC, both for advance and premier customers.

All the others seem to apply some fee regardless of the fee choice of the sender. My company in HK always sends my salary via SWIFT with OUR as fee, but when I was receiving it in Cathay United (better FX rate overall), the bank was still charging me ~USD 6 for crediting notwithstanding the OUR fee.

HSBC instead credits in full if sender does OUR, but they call you each time you receive a crossborder transaction to verify the purpose (with Cathay I could do that online or via app), the funds are credited immediately after the call, and after a few days they send to your registered address a confirmation letter for the incoming transfer credit. Very bureaucratic and wasteful from their side, but all is free of charge, they get it a bit back with a slightly worse FX rate.

For 玉山:

Regular account: Sending as OUR they won’t charge an incoming fee. For SHA they charge up to 1700NT (base + percentage formula).

Premier account (>300萬 invested in their fund management): They wave incoming swift fees and give one free outgoing swift transfer per month. But you end up paying much more back through their 1-2% management fees so you lose money in the end. Better to just pay the fees and don’t get suckered into their fund management like me.

For 玉山 it’s time consuming that they have to call me each time even when I told them to put on file to automate it. But sometimes it’s a call from my favorite banker.

For my TW business account, I don’t have to go with my ID in person. For my personal account, I have to go in person with my ID. Though they made an exception and said I could email my ID when I did a $100 test transfer to my personal account. Must be the difference between foreigner and local person.

I use 玉山 because they have much better rates for VIP customers. Check out their ‘App’ rates here, and you can negotiate better if you have a relationship: 外幣匯率 - 玉山銀行

This reduces the normal USD/TWD buy/sell spread from 0.1 down to 0.03 for regular app users

I can also confirm that with Cathay United, I could receive personal account swift transfers online as a foreigner without having to go through a phone call.

Mega Bank didn’t apply a fee the last time I did an OUR SWIFT transfer with Wise, though they have on previous occasions.

They also haven’t called me with my last couple of transfers, but I tend to not pick up the phone anyway, and in the past the transfer has still gone through even when I missed the call. ![]()

very random ahaha

Just to confirm this, are you saying you sent from Fubon Taiwan to IBKR US and there was only a 12.5 USD intermediary fee? Sending to IBKR’s Citi account from Hua Nan I got an intermediary fee of 20 USD. May I ask which of IBKR’s bank accounts you sent to? They have Citi and US Bank and it’s random which one they assign to you. My wife is US Bank and I’m Citi.

I am Citi too and it is more like 20 or 25 USD taken out by Citi.

Is it Citi though? My understanding was that it will have been taken by an intermediary bank

@marcopoloTW executed a withdrawal from IB to Taipei Fubon. Opposite direction.

It may be an intermediate bank and I am not sure.

Has anyone attempted to file a lawsuit against any banks in this area?

I am familiar with a lawyer in the United States who recently initiated a lawsuit worth 300 million USD against an American bank, which eventually escalated to a 6 billion USD lawsuit .The reason behind the lawsuit was that the bank had failed to close his accounts even after he requested them to do so, and continued to harass him after he sent multiple cease and desist letters. This is not a class-action lawsuit but rather a personal dispute between the individual and the bank. The lawsuit initially started with a demand for immediate closure of the accounts and a ban on any future contact, but the amount increased to 300 million USD as the individual grew frustrated with the bank’s persistent harassment, and finally to 6 billion USD when the bank made further attempts to contact him. The bank would be solely responsible for paying out any damages if the individual wins the case, not the government.

Taiwan has anti-discrimination laws, which can easily be used to challenge the bank’s discriminatory policies. Although it may not result in the same amount of money as in the case mentioned above, suing the bank can still be a fulfilling experience as it would force them to change their policies and possibly even result in a compensation.

I don’t know - but these damages seem quite excessive compared to the damage inflicted to the person. I doubt that you would be able to successfully sue a bank for that much money outside the US. Some thousand NT$ - maybe. But millions and billions…?

Do you still use this method? Are you on IBKR Lite or Pro? Is the intermediate bank and fee the same still? No additional fees from IBKR (once a month) or Fubon?