No one it seems, but when asking to MOF the reply was you are not resident until you stay 183 days in, so STFU dirty foreigner.

That’s it

No one it seems, but when asking to MOF the reply was you are not resident until you stay 183 days in, so STFU dirty foreigner.

That’s it

Even where it is standard. This would apply to both foreigners and citizens

this, I wouldn’t bother if citizens and alien residents are treated equally, but this is not the case. the DTAs and the Income Tax Act itself are written in a way not to create differences based on nationalities and the DTAs language is very clear (it is very clear in English for the Canadian, Australian, New Zealand and UK ones and very clear in Italian for the Italian one) about not having citizens of one country to have any different requirements to establish tax residency from those of the other country (so an Italian, like me, in Taiwan should be treated as a Taiwanese for tax purposes, and viceversa)

I started going through some of them the other day and making a file. It’s also pretty clear in the DTAs for India, Indonesia, Israel, Japan, Singapore, Thailand, Vietnam, Kiribati, Gambia, Senegal, South Africa, Swaziland, and Paraguay.

I didn’t recheck the ~16 European ones yet, but from memory most (not all) had clear non-discrimination clauses that should cover this situation.

Less so for Malaysia (refers to “residents” not nationals/citizens, Saudi Arabia (no non-discrimination clause), Australia (doesn’t seem to have a non-discrimination clause), New Zealand (doesn’t seem to have a non-discrimination clause, but does have an annex indicating that discrimination is “undesirable”), and Canada (doesn’t seem to have a non-discrimination clause for individuals).

A bit harsh I doubt they called you a dirty foreigner lol maybe just a tall one lol.

I hope they change it for arc holders to the same as citizens. Good luck with your endeavors.

Most countries definitions are more nuanced than this. If you can demonstrate residential ties then you can usually become a tax resident even if you reside less than 183 days. The UK even has specific automatic tests such that if you were tax resident in previous years you are probably presumed tax resident in the next year.

In Italy it is very clear (for once): when a foreigner gets a permit to stay in Italy, he must report to the town hall and register him/herself as resident in that town. Once that foreigner is registered as resident, then the foreigner has obtained de iure tax residency and now is tax liable and has instead the burden to demonstrate the non tax residency.

The same principle should apply in Taiwan, once you get ARC (so generally speaking residency permit for more than 1 yr) you should be considered domiciled and tax resident, with the domicile being the address indicated on the A(P)RC and have then the burden of proving otherwise.

I’ve noticed this about the Canadian one while reviewing it this morning. It only contains a non-discrimination clause for businesses. But I think one can still request to have the tax residency determined under the DTA by the Mutual Agreement Procedure.

Yeah, sure, I’m just saying that the language isn’t clear in these cases and there’s nothing explicitly prohibiting discrimination like there is in the other DTAs.

Of the four larger companies I’ve worked at in Taiwan, two withheld the 18% for 6 months every year starting in January, and the other two didn’t. I went over this in another thread, but in 2022 I sorted out all the relevant policies and even contacted the tax office and confirmed that it wasn’t necessary for my employer at that time to withhold, but they still wouldn’t budge. Eventually I left that company, and where I work now they don’t withhold.

This article is interesting for those who don’t want their employers to withhold:

https://www.chihyun0917.com.tw/product-detail-2625394.html

如果是因為職務或工作關係預計在一課稅年度內可居留滿183天者,自始即可按上開「居住者」扣繳率扣繳,如離境不再來我國時,其於一課稅年度在我國境內實際居留天數合計不滿183天者,再依上開「非居住者」扣繳率核計扣繳稅額,就其原扣繳稅額之差額補徵;如護照或居留證所記載居留期間於一課稅年度內未滿183天者,扣繳義務人則應按上開「非居住者」之扣繳率扣繳所得稅款。

GPT Translation:

If it is anticipated due to the nature of the job or work that the employee will reside in Taiwan for a total of 183 days or more within a taxable year, the withholding from the start can be according to the “resident” rate. If the individual leaves and does not return to Taiwan, and their actual total days of residence in Taiwan within a taxable year are less than 183 days, then the withholding should be recalculated according to the “non-resident” rate, and any difference in the originally withheld tax amount should be additionally collected. If the period of stay indicated in the passport or resident certificate is less than 183 days within a taxable year, then the withholding agent should withhold income tax according to the “non-resident” rate.

Essentially, if your employer anticipates that you will stay in Taiwan for a total of 183 days this year, they can withhold you at the regular resident rate, instead of 18%, according to that article. If your contract is for 1 year, and you only have like 20 something days of annual leave, then you could argue that they anticipate you will be in Taiwan for at least 183 days that year.

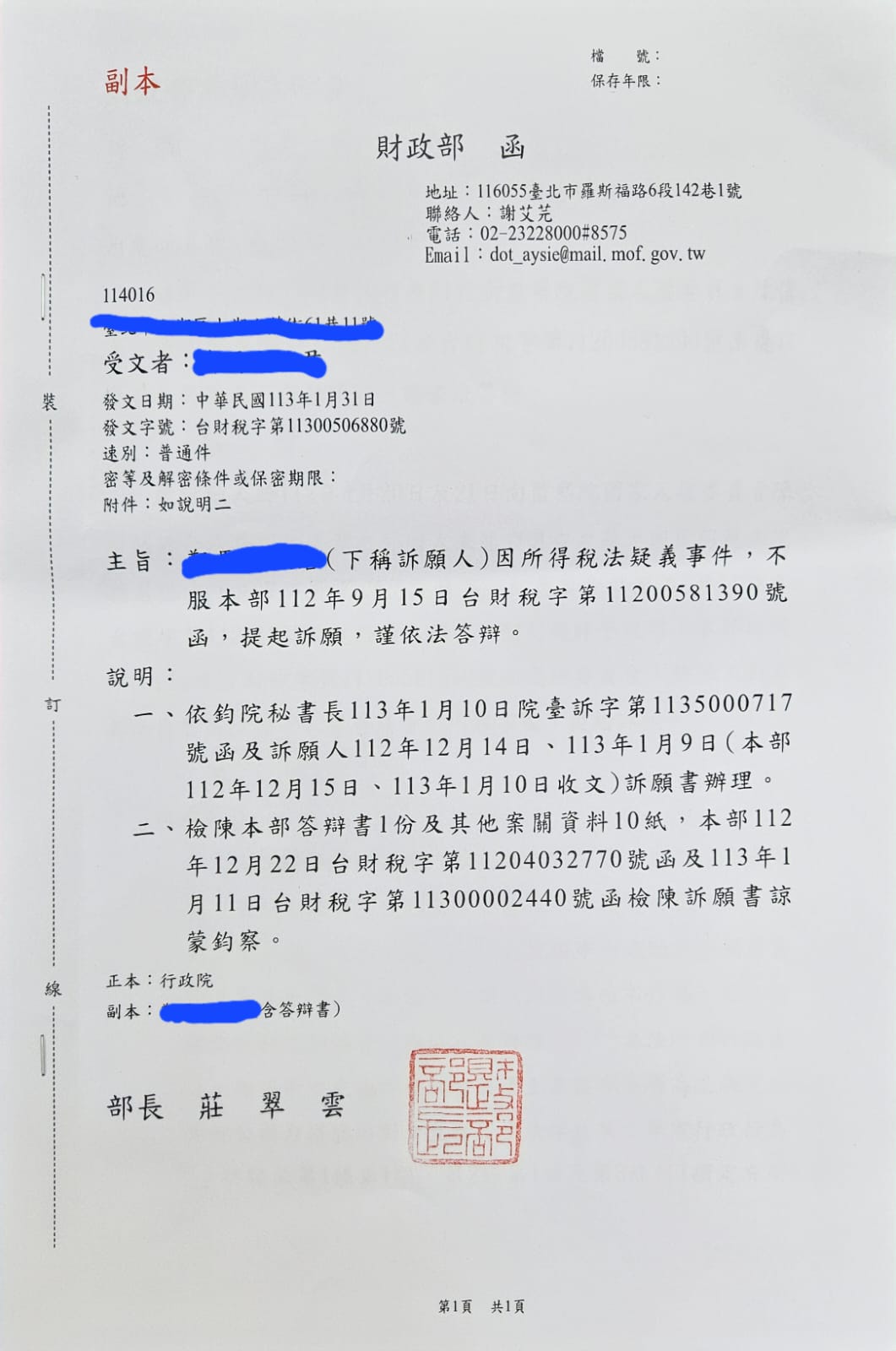

OK folks, ready for some more nonsense? But this time they put some more effort in covering their asses:

Summary:

This is the reply to the administrative appeal I submitted before Christmas in reply to their BS answer they gave to the Human Rights Commission. This is not the reply to the official diplomatic inquiry the Italian Office sent them in January,

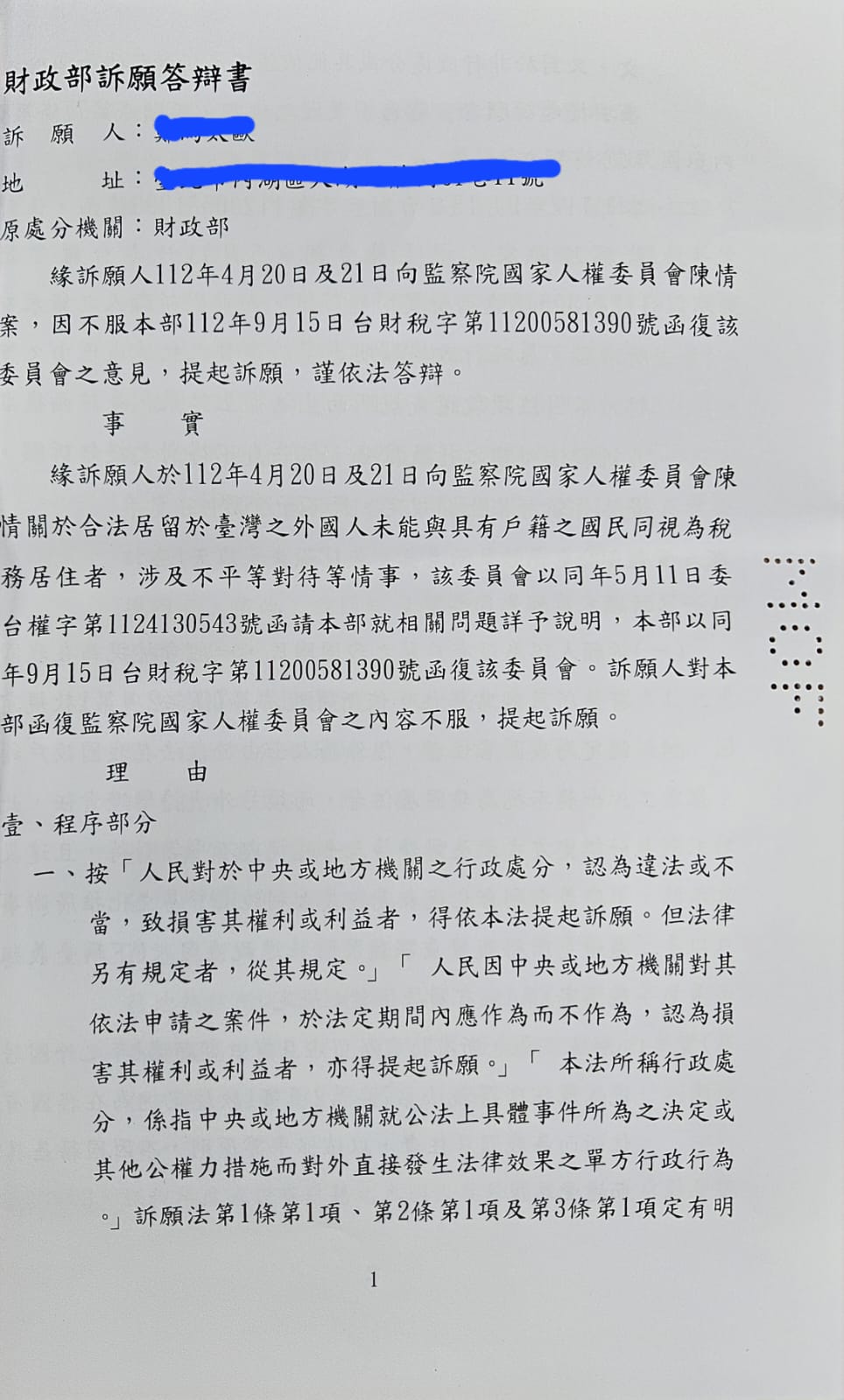

First they didn’t accept the appeal on the grounds of their letter to the Human Rights Commission was not a decision or administrative act, so the complaint can’t be accepted according to the provisions of the Administrative Appeal Act (according to the various experiences now, it seems that it is interpreted VERY narrowly only to decision directly affecting someone individually and specifically, like fines basically).

Then they go on explaining why they still defend their interpretation of domicile and why foreigners can’t be considered as such and why the Italian DTA anti-discrimination clause is not applicable here.

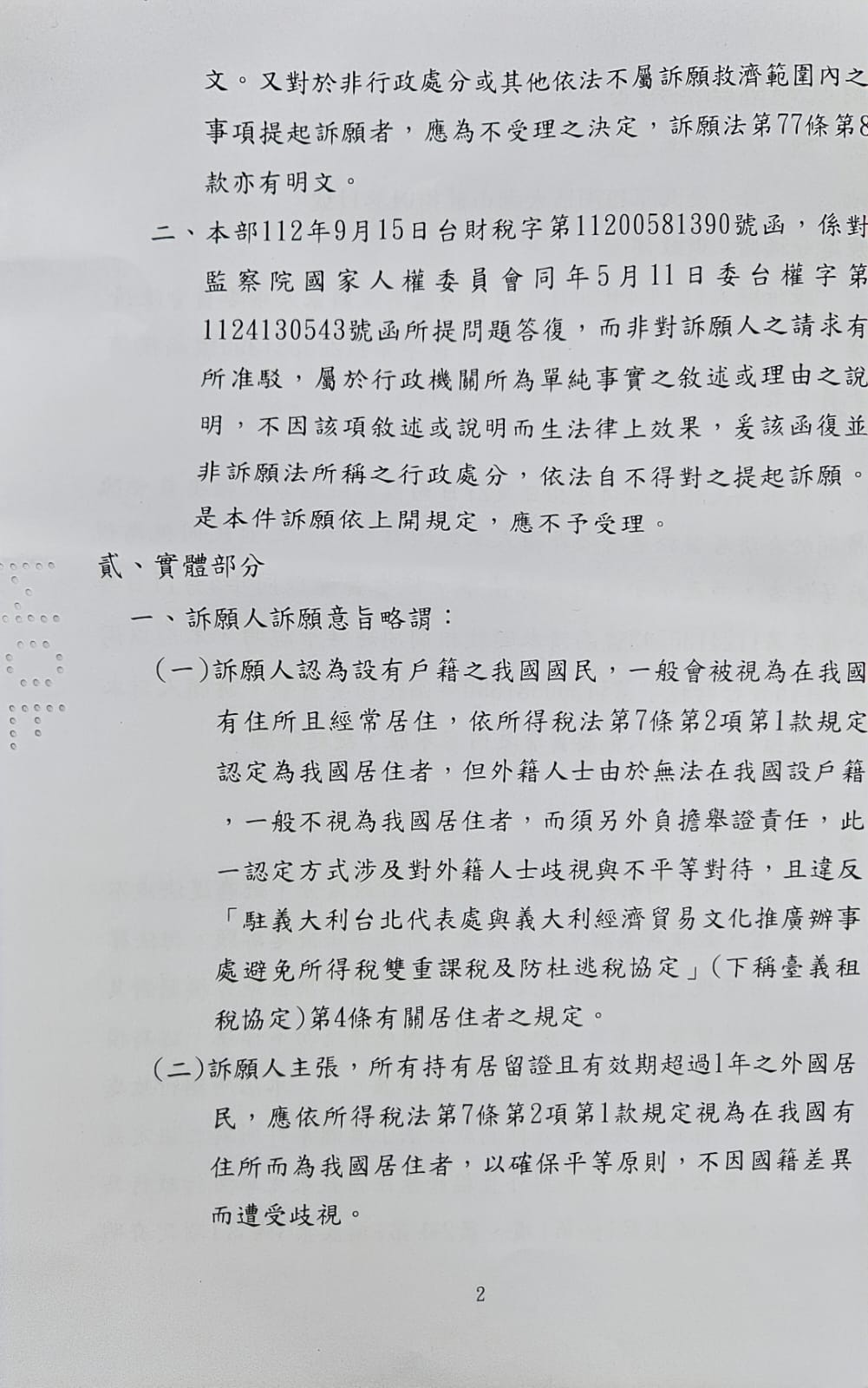

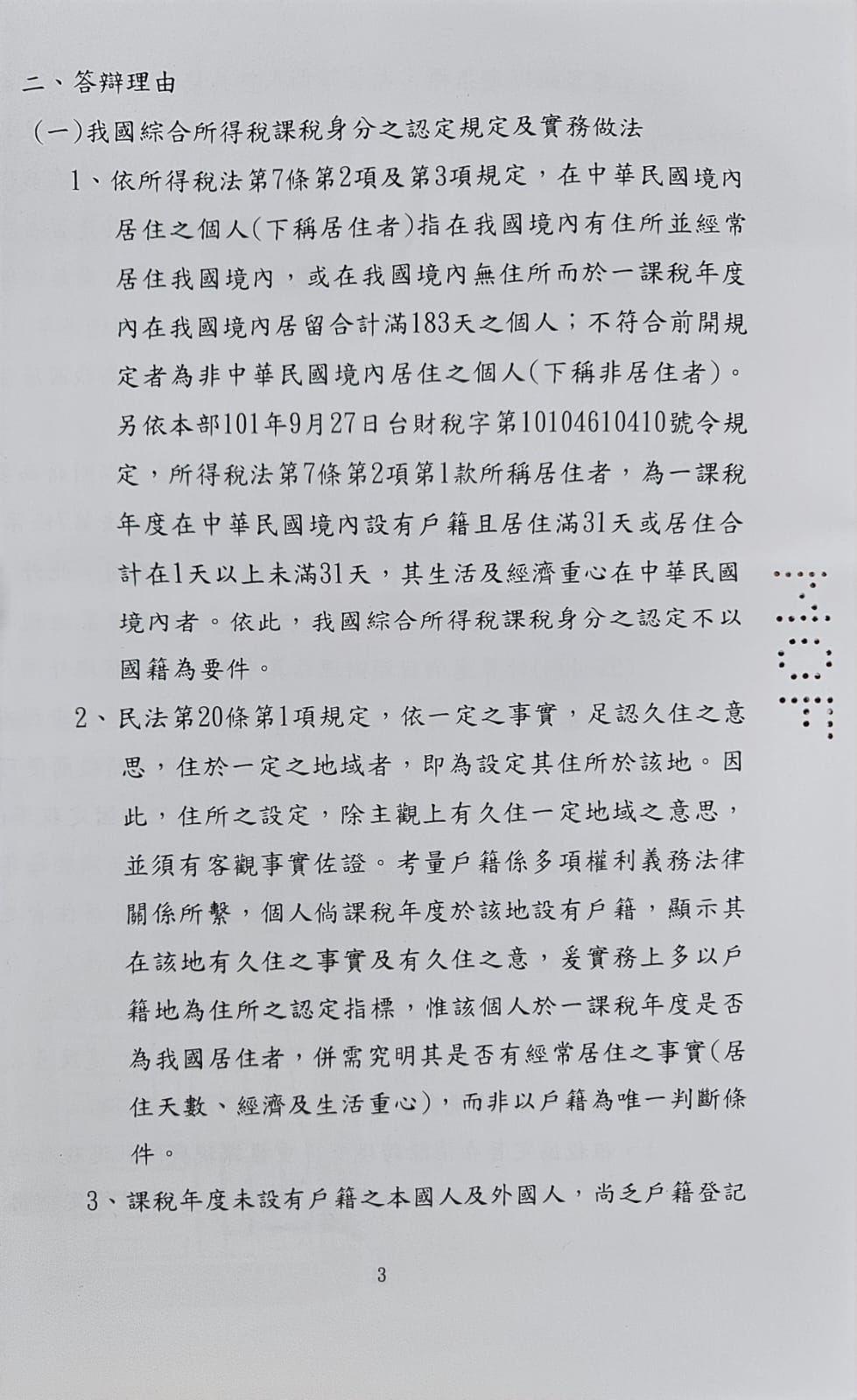

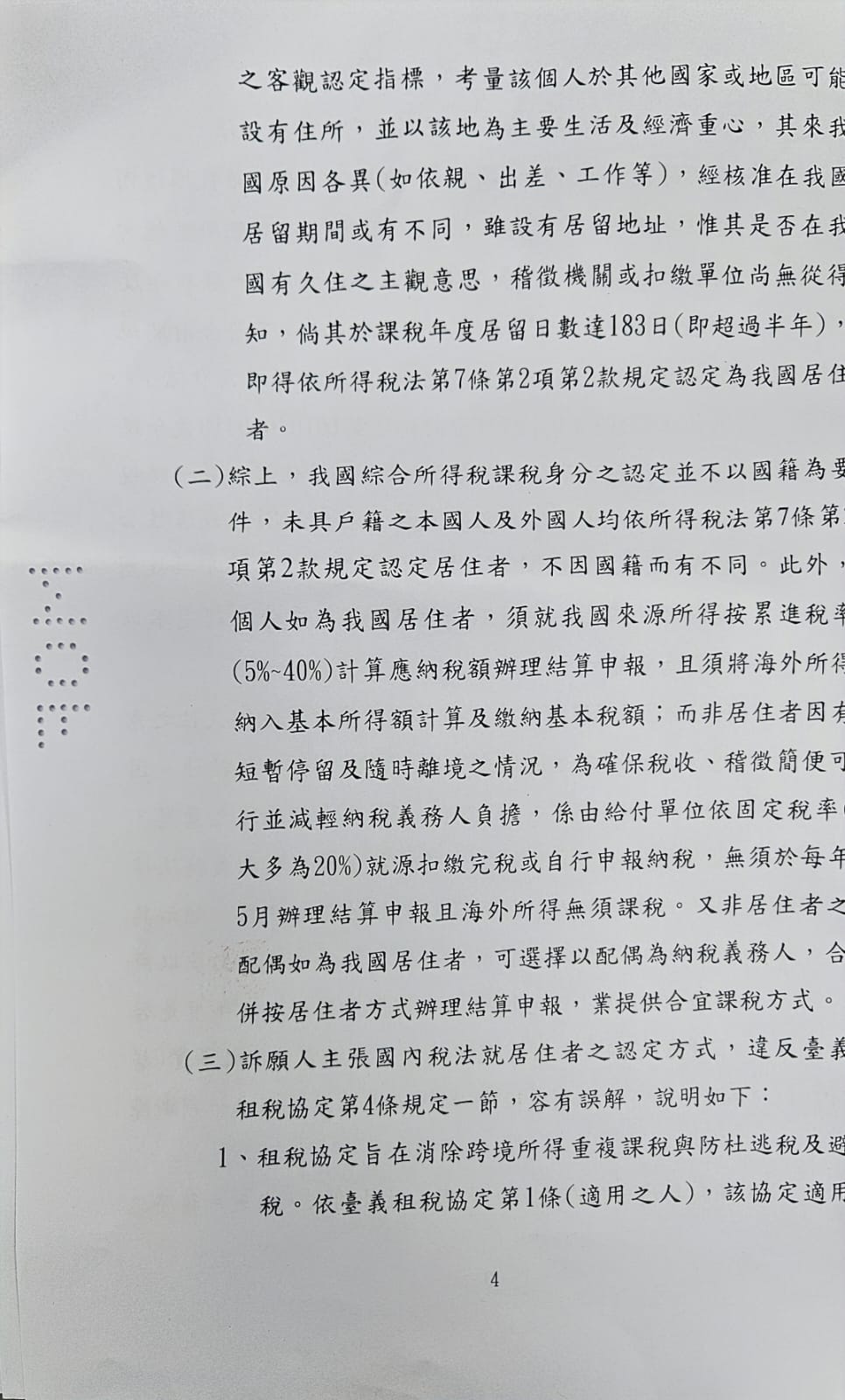

So first they say that according to an order of the ministry of finance (year 2012 order 10104610410) to be considered domiciled (and hence deemed as tax residents) as per Income Tax Act (ITA) art. 7 par 1 sub 1 an individual MUST have household registration and spend 31 days in the country per tax year: if staying between 1 and 31 days with HHR and having centre of vital interests in the country also must be considered tax resident. Otherwise, if no household registration, then there is the test of the 183 days per calendar year (art. 7 par 1 sub 2 of ITA). Anyone else is not to be considered as tax resident.

then they refer to art. 20 of the civil code ( 依一定事實,足認以久住之意思,住於一定之地域者,即為設定其住所於該地。一人同時不得有兩住所。) They basically consider here only HHR as supportive fact and don’t give a flying fuck on the other “vital interests” and always suppose that foreigners will eventually leave, like Taiwanese instead are chained to the ground…

This is reiterated in the first paragraph of page 4 (starting at the bottom of page 3 of the explanation) where it says that even though foreigners can’t have HHR and hence some other factors may be used to ascertain the domicile, the “tax authority has no way of knowing whether they (the foreigners) have the subjective intention to stay in (the country) for a long time.”…

second paragraph of page 4 of the explanation is so silly, they seem so satisfied and happy with their nonsense (google translated): “the identification of comprehensive income tax status in China does not rely on nationality. Both locals and foreigners without household registration are recognized as residents in accordance with the provisions of Article 7, Paragraph 2, Paragraph 2 of the Income Tax Law, and nationality is not required. And there is a difference. In addition, if an individual is a resident of China, he or she must calculate the tax payable on income from sources in China at a progressive tax rate (5%-40%) and make a settlement declaration, and must include overseas income in the calculation of basic income and pay the basic tax; non-residents Due to the short-term stay and the possibility of leaving the country at any time, in order to ensure that taxation and collection are simple and feasible and reduce the burden on taxpayers, the paying unit will withhold the tax at the source or declare the tax on its own according to a fixed tax rate (mostly 20%). There is no need to file a settlement declaration in May every year and there is no tax on overseas income. If the non-resident spouse is a resident of my country, he or she can choose to make the spouse the taxpayer and handle the settlement declaration in the same manner as a resident, which provides a suitable taxation method.” So even blatantly saying, rely on your Taiwanese spouse if you have to handle your shite since you can’t…

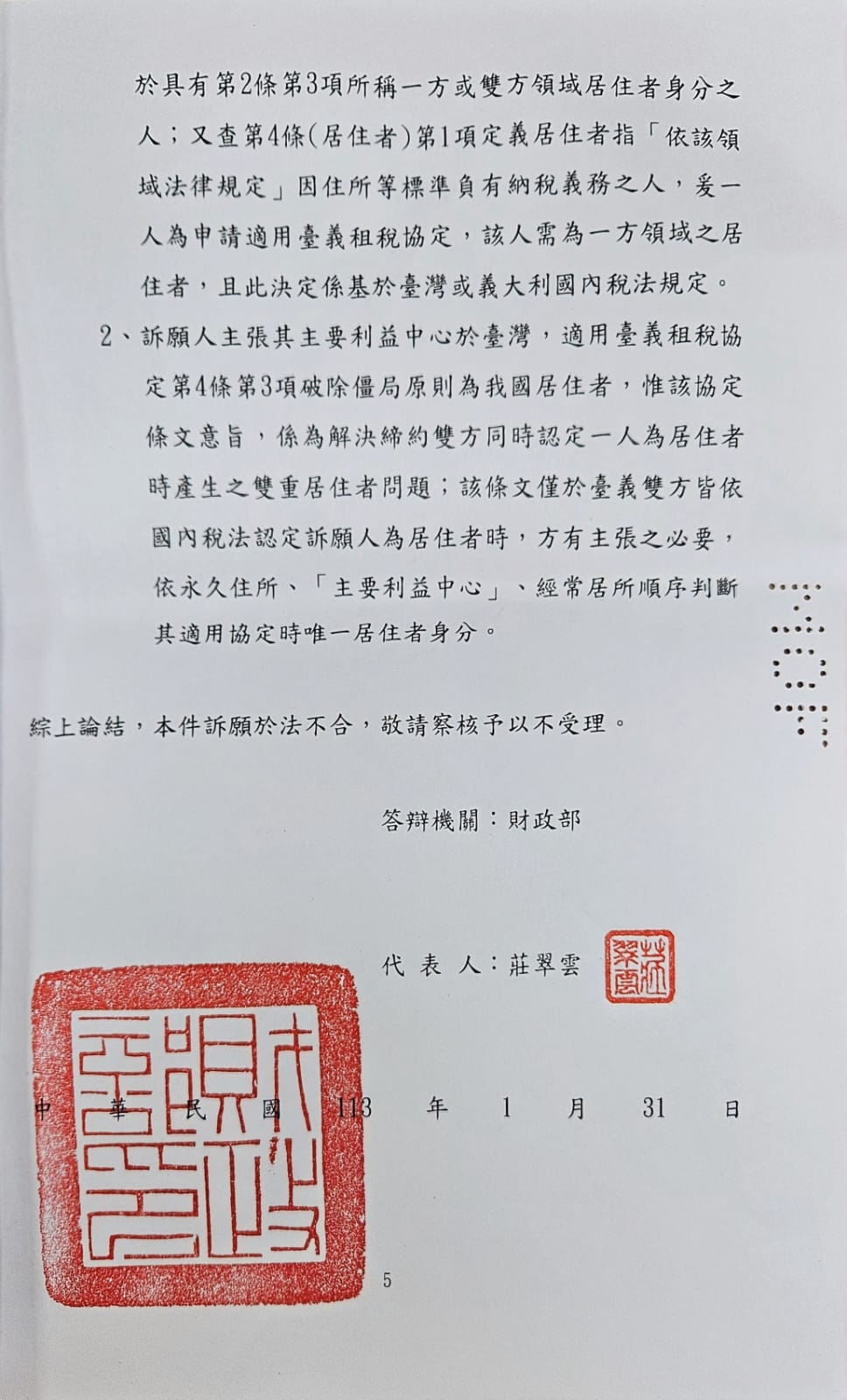

Regarding instead my claim that their policy is violating the non-discrimination clause of the DTA with Italy, they went on saying that the tax residency is assessed based on the regulation of the respective countries and the “deadlock-breaking” principle of centre of vital interests is just to resolve cases where tax residency cannot be assessed based on normal criteria…

I am speechless. Will send this to my consulate and my counterarguments.

Hi Andrew,

I’ll reply to you as there are just way too many side arguments that my initial post sparked and I don’t have the time to engage with everyone. You are also probably the most interest in constructive change here.

I agree with you that the withholding situation is not ideal. That said, it isn’t terrible. If you consider time value of money, the delay to get your refund only increases your effective tax rate by a small fraction of a percent. Again, I agree there is room for improvement here.

Regarding CRS, that’s a bank thing, and yes you are not technically a tax resident in Taiwan until you spend your 183 days here. Having have filled out many CRS forms for banks in various countries, I can tell you that they generally keep your tax residency the same until you fill out an update (which you must do if your situation changes). Perhaps the Taiwanese banks are different, but I haven’t had to fill out a CRS form here and this is more of a bank issue rather than a government issue.

Anyway, to the bigger point I was going to make with my initial post.

What is the biggest pain point?

I ask this because based on my reading and the push to get tax residence quickly suggests that some of the contributors here are digital nomads just looking for a cheap and easy tax residence certificate in a low tax country so that their high tax home country doesn’t tax them. Then they piss off to Bali, Thailand, Colombia, etc. I used to be a digital nomad and can smell my own. This was a major issue. Tax residency certificates with low minimal stay requirements are not easy and/or expensive. Taiwan would blow all other offerings out of the water if a gold card holder (easy to get) can get an easy domicile here and then only spend 31 days a year in Taiwan.

I point this out because a change like this will probably be much harder to pass as someone along the way will realize what a global tax loop hole they are creating. It would also generate some negative attention to the island. This is why I suggest a different solution based on the actual biggest problem of people who actually live here. If withholding is the biggest problem, then I feel like pushing for a change in that or better enforcement of companies withholding the correct/adjusted amounts after such that your annual withholding would match what you ultimately owe. But the solution should come once the pain points are understood, and ideally would not require minimal legal changes so it doesn’t take years.

Finally, a point on fairness of the 31 day tax residency if domiciled rule. The rule isn’t intended to give Taiwanese an advantage. It is more of a catch all to make sure Taiwanese people pay their taxes if they maintain a connection to Taiwan. I see absolutely no problem with this.

I wonder whether Article 22 of the Civil Code is relevant here:

A person’s residence is deemed to be his/her domicile in either of the following circumstances

(1) when his/her domicile cannot be certified.

(2) when he/she has no domicile in Taiwan except when lex domicilli governs.

I have no domicile in Taiwan, or my domicile cannot be certified because I don’t have HHR, in which case isn’t my residence deemed to be my domicile? I don’t really know what that means actually. ![]()

I’m a Canadian citizen who hasn’t lived in Canada for 7ish years and this will be my first year filing in Taiwan… I’ll be glad to jump on the bandwagon and lodge complaints with my representative office.

That said, it isn’t terrible.

If your tax witholding is ~5% in December, and then jumps to 18% in January, that is extremely terrible.

and will see the money only in ~18 months…

Wow. Their reply is beyond outrageous.

The Canadian and British tax agencies have very clear ways of knowing whether a foreigner has the intention of staying for a long time and therefore determining tax residency status on the basis of cirucmstances… the idea that Taiwan’s tax agency can’t figure this out is utterly ridiculous.

It’s a bank thing, true, but I think based on the NTB’s policy as well. As in, if we’re not considered tax residents in Taiwan for the first 183 days of each year, and we’re not, it’s reasonable for banks to ask where else we’re tax-resident, even if we’re not tax-resident anywhere else. (I’ve yet to hear of a government department or bank etc. agreeing that “nowhere” is an acceptable answer to this question.)

I’m surprised you’ve never had to fill out CRS forms here, unless you opened all your bank accounts in Taiwan before CRS came into force (2019?). We have the other thread about that, but it’s the norm that foreigners are forced to fill these out incorrectly.

I don’t think that’s fair. Most (all?) of us complaining about this here are doing so because we genuinely live here by any definition and stay >183 days anyway. I’ve been tax-resident in Taiwan under the current definition since 2017 and have an APRC.

I’m not looking for cheap and easy tax residence, just to get the fact that Taiwan is my center of life etc. recognized, because it is. It’s more about the principle for me. (I don’t even have a local employer withholding 18% tax from me.)

I get what you’re saying about gold card holders etc. and I suppose that’s a valid concern… but I don’t think it justifies incorrect treatment of all the other foreigners who genuinely have Taiwan as their homes.

I don’t see anything suggested as some global tax loophole. It’s really just centered around acknowledging that resident foreigners can be properly resident here, as they are in other countries. It’s not that weird to expect residents to be treated consistently as residents, IMO.

Let’s do some math with a simplified example. Your withholding should be 12% toward the end of the year (your marginal tax rate) if there was no 18% withholding to start. So you save a bit on the second half of the year. Now, let’s say you make 100k a month for simplicity. You’d pay 39200+640k12%=116k in taxes. If they withhold 18% for your first 6 months then 5% for your second 6 months, you pay 600k18%+600k*5%=138k. That’s about a 22k difference that they overcharged you. Even if they held that money the full 18 months until your refund, the interest on it would only be about 660nt assuming a 2% rate. Even if you get a 5% return in something more aggressive, your loss is about 1650nt, or an increase in effective tax rate of 0.14%. Not terrible, unless maybe if you live paycheck to paycheck.

Note that this is a simplified example, and a more complicated one would take into account the fact that you are having more withheld earlier rather than later in the year. However, that would not change the outcome all too much. Feel free to spreadsheet it out.