I could say the same about your “refutation.”

I thought so. Anyways… anonymous forums are often a better place to talk about one’s financial successes and failures since some folks in the real world can be pretty petty and jealous of others’ success. So brag on! ![]()

If you had stocks that had the same overall return, you don’t see why a dividend aristocrat would attractive to investors, and think a dollar is a dollar, like the article? You don’t see why the long term, steady flow of cash would be attractive to the proverbial gramma with her div stocks, vs riding the ups and downs of the market? Hell, with the same returns, that should be more attractive to most long term investors (those that think they can time their moves well will like volatility better)!

The above is a completely different subject.

Swedroe is not claiming dividend stocks are useless. But the reasons for buying them are behavioral. Again the main point is that dividends are not the same as an interest payment. When a stock pays an x% dividend, it does not result in an x% increase in total return at the time payment is received. One has no additional money or income. Whereas when interest is paid on a bond that is immediately an increase in total return/income.

One has received no extra money when receiving a dividend unlike an interest payment.

That is nowhere near the same as receiving dividends for the purposes you describe in your post. Those are behavioral issues. Nothing wrong with wanting some semi-reliable cashflow. But again, because a stock pays a 4% dividend one should not think that is the same as an additional 4% return or interest payment. As I said above many retail investors think that is exactly what is happening… they have the mistaken idea that they are getting extra money with a dividend payment.

In non-taxable or tax deferred accounts yes, but not in taxable so it’s not a universal attraction. And the empirical evidence does not seem to support it, but again, that is a completely different issue from what’s being discussed here.

So yeah, I agree with what you posted above from the standpoint that dividends can certainly be desirable for a lot of folks, for the right reasons.

So investors are saavy enough to bid down prices due to dividends (only to bid them back up later), but not saavy enough to do so with a discount for taxes. Interesting argument. ![]()

It seems to me it’s more typical that investors do the opposite of what you claim - they quote the prices without taking dividends into account for total returns.

Nope. Merely said that there appear to be advantages and disadvantages to receiving dividends depending on the type of account they are situated in. And I already stated that investors don’t need to bid down prices due to dividends. The exchanges and market makers have already adjusted the opening prices. As I said before anybody can verify this for themselves by looking at price history and ex-dividend dates and payouts.

If that’s what a typical retail investor does then they are incorrectly calculating their total returns, obviously. (If I understood what you are trying to say… are you saying investors exclude dividends when calculating their total return??? That’s like a stock splitting and not taking into account that you have more shares [or less in a reverse split]. Makes no sense.)

You can state it, but that’s not how it works (other than market makers also bid prices up and down) - prices aren’t just set by the exchanges.

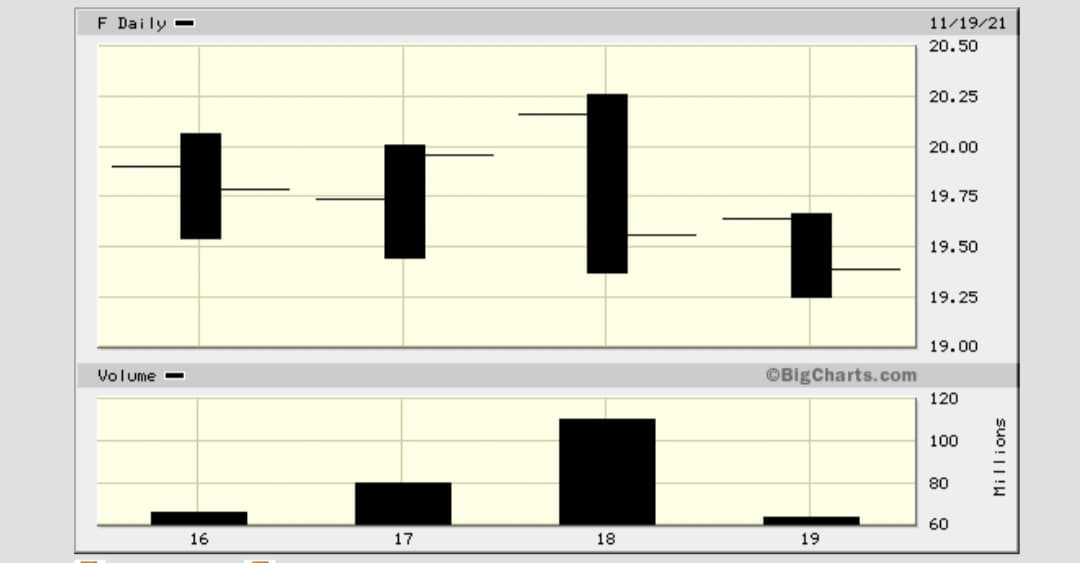

Yep - and they’ll see that’s not how it works. This is F, which went ex dividend on 11/18 for a dime. Show me where the exchanges adjusted the open price down to account for that

Yep. I’d wager most investors simply look at the price charts for the performance of a given stick, which doesn’t include dividends. Charts do account for splits.

This is what Fidelity says about ex-dividend dates and the payouts:

"A stock price adjusts downward when a dividend is paid. The adjustment may not be easily observed amidst the daily price fluctuations of a typical stock, but the adjustment does happen. This adjustment is much more obvious when a company pays a “special dividend” (also known as a one-time dividend). When a company pays a special dividend to its shareholders, the stock price is immediately reduced. "

And

"You may wonder if there is a way to capture only the dividend payment by purchasing the stock just prior to the ex-dividend date and selling on the ex-dividend date. The answer is “not quite.”

“Remember that the stock price adjusts for the dividend payment. You buy 200 shares of stock at $24 per share on February 5, one day before the ex-dividend date of February 6, and you sell the stock at the close of February 6. The stock pays a quarterly dividend of $0.50 per share. The stock price will adjust downward on February 6 to reflect the $0.50 payment. It’s possible that, despite this adjustment, the stock could actually close on February 6 at a higher level. It is also possible that the stock price could close February 6 at a level lower than the $23.50 price suggested by the $0.50 adjustment to reflect the $0.50 dividend.”

Earlier I posted a link to Vanguard saying virtually the same thing.

Once again, if dividend paying stocks were paying extra money in the form of a dividend over a non-dividend paying stock, then they should offer higher total returns than non-dividend stocks, but this appears not to be the case.

1 Like

Yes, there’s an adjustment because investors take it into account and might bid differently. Not because the exchanges change the price on open as you claim. And per your article, it might not be easily seen - if it were just set as a delta to dividend price (as you claim), it WOULD be easily seen. As you can see from the chart included, F traded UP on open on its ex div date, contrary to your claims about the exchanges setting the price on open. Prices can be different on open compared to close because of post/pre market activity driving the prices, not because the exchanges set them to something else. You don’t know how this works, AT ALL.

Btw, that article is wrong on a very basic point:

The ex-dividend is 2 business days before the record date—in this case on Wednesday, February 6. Anyone who bought the stock on Tuesday or after would not get the dividend

It seems to me you two are arguing semantics at this point. Markets consist of buyers and sellers who are collectively agreeing on a price adjustment after a dividend. Otherwise there’s no exchange.

Some sources claim it’s an exchange rule others claim it’s market forces. For sure, even if market makers set an opening price there is no guarantee the stock will open at that price if there is more or less demand for the stock.

Regardless of the mechanics (which is a side issue), it still stands that dividends are simply not the same as an interest payment. An investor’s profit is not being increased by the amount of the dividend payout.

He seems to me to be claiming that the exchange, outside the normal bid / ask process, adjust prices.

What source?

Nobody said it was the same. Nobody even made the analogy, other than you.

Well yeah, they adjust it to the new lower price that buyers are willing to pay.

No, he’s explicitly claimed that the price at close is adjusted by the div price to make the new open price. Now he’s saying that might be an exchange rule. This isn’t just semantics.

“On the ex-dividend] date, the stock price is adjusted downward by the amount of the dividend by the exchange on which the stock trades.”

"Lichtenfeld says the strategy doesn’t work because of that rule requiring stocks to go down by the amount of the dividend on the ex-dividend date. This, Lichtenfeld believes, creates “too much risk that the stock would fall as much as the dividend paid or more.”

I have found more sources claiming this. Whether it’s accurate or not, I don’t know. Obviously market forces can easily override whatever a market specialist sets as initial bid/ask prices. I have also heard from market specialists who claim that is what they do. But never interrogated them about it.

JD Smith appears to believe that dividend payments behave like an interest payment in the sense you are getting “extra” money. When in fact you are not.

Edited to add:

Many retail investors think that if a stock pays a 4% dividend they are getting 4% more money. That is simply not the case. Thus the interest payment analogy, because that IS how many investors look at dividends.

1 Like

That is how adjusted closing price is calculated. Initial closing price does not account for the dividends, so that is then factored in.

Adjusted closing price doesn’t set next day opening price.

In any case, the dividend is a guaranteed return separate from (even if related to) the movement of the stock itself. You can look at stocks and ETFs whose NAV is relatively flat year over year, but they’re paying an 8% dividend or something, and if you own it you’re getting 8% +/- the movement of the stock price.

Likewise if a stock has gone up 10% while paying an 8% dividend, you made 18%

I don’t know if the stock adjusts after the dividend or not, but to me it doesn’t matter, as over the longer term the stock moves in one direction and then the dividend is paid out as well. Whether the dividend is preventing the stock from moving higher than it otherwise would (which makes sense, they’re paying out dividend rather than keeping it in the bank), you still do have dividend + movement of the underlying.

none of that sets opening price.

none of that sets opening price.