Just make sure you check the right E.Sun rate - they have two rates: One “normal” rate and one preferential rate (for online transactions). But the app will still show the “normal” rate in some places… Do not choose “Foreign Exchange Rates” in the app - that will show the wrong rate…

That should be the right one (notice the very low spread between buy and sell):

That never worked for me (the designated FCY account just doesn’t show up in the app) - I always have to call them. But then it’s very easy: I just tell them to transfer the money to my designated account at E.Sun and they take care of the rest.

I have finally joined the world of HSBC so I will probably have some data to share eventually.

Got my US Premier account approved yesterday. Wasn’t sure if I should pretend I was in the US using a VPN, but luckily they have an application process for folks outside the country who fit a certain criteria, which I do. So that worked out.

Now I’m attempting to set up accounts in Singapore and Malaysia, which is the entire reason for doing any of this to begin with. I’ll be in each country over the next two weeks so I’ll do it in person if necessary, but it seems there is a process to do it remotely.

And of course, I could also open a Taiwan account some time.

Supposedly they will. I’m in the process of attempting it so will let you know maybe in a month or two to confirm! But multiple people from within HSBC as well as random data points on the internet do suggest that it is possible.

Benefit is purely because I have businesses in both of those countries and would like to be able to pull the money out with more flexibility. Despite having the businesses and business bank accounts, no other bank* thus far has allowed me to open a personal account in either of those countries without some visa/residency.

*actually DBS and standard chartered have also informed me that I could do so under their VIP/premier programs, but I have chosen to try with HSBC first because I was able to open a US premier account online, from Taiwan, and do so without significant deposit (using their recurring ACH qualification)

If you have reasons they generally open it for you. Heck, opened a HSBC UK account despite I have never lived there, not a Brit, only connection is that my employer has an officer there and (like twice ever) sometimes I go there for biz to meet with partners. Used that excuse for reimbursements, and presto they opened the account for me.

We do not have any biz in Singapore nor Malaysia, so though luck.

Often, using an ATM to withdraw cash is also suggested as an alternative to wiring money internationally via SWIFT.

However, the VISA exchange rate (which will be used in those cases) also includes a hidden markup - check the VISA rate here (although that’s a US website, my European bank used exactly the same rates):

To be fair, the VISA exchange rate is only set once per day (?) - so it might actually be better in case of falling exchange rates in some scenarios. However, you never really know when exactly the transaction will settle (in my attempts it took between 0-2 business days).

Overall, there is no “free lunch” with ATM withdrawals either. In the end (at least for EUR-TWD), the VISA rate is slightly worse than E.SUN’s rate - which often offsets the cost of a SWIFT transfer for larger amounts.

Understandable, of course, as no bank wants to do business for free. But it’s still wrong to claim that ATM withdrawals are “completely free” and only SWIFT transfers cost money. They’re just better hiding the fees in the exchange rate.

For small transactions, though, nothing will beat the ATM (especially considering convenience)…

(Given that, of course, one’s bank doesn’t charge a ATM fee, the ATM doesn’t charge an ATM fee and one doesn’t accidentally accept the DCC “offer” of the ATM…)

HSBC’s rates might still be a tiny bit better than the VISA rate, though.

Are people who use HSBC happy with their service?I’ve seen mixed reviews on Reddit. Seems like using HSBC to get the money from the US to Taiwan makes sense but the jury is still out on using HSBC to convert to TWD vs transferring USD to a local TW bank (like ESun) then converting there?

Using the Global Transfer (and accepting the slightly worse FX rate) is definitely much more convenient (and faster!) than a SWIFT transfer.

I still feel like the branch staff (at least in the branch I was visiting) were less friendly than the ones at Cathay or E.Sun. I felt more welcome at the other banks than at HSBC (the HSBC branch felt more like a police station to me…) - even though I am a Premier customer there. Except for the Global Transfer, that “status” is basically worthless. For example, Cathay and E.Sun allow walk-ins for account opening - HSBC requires an appointment.

HSBC’s phone service is very smooth, though.

In the end, they’re just a bank like any other. If you manage your expectations, then I guess one can be “happy” with them…

Update: It’s actually possible to do the transfer without calling them: One has to use the website for this and not the app

And - another update:

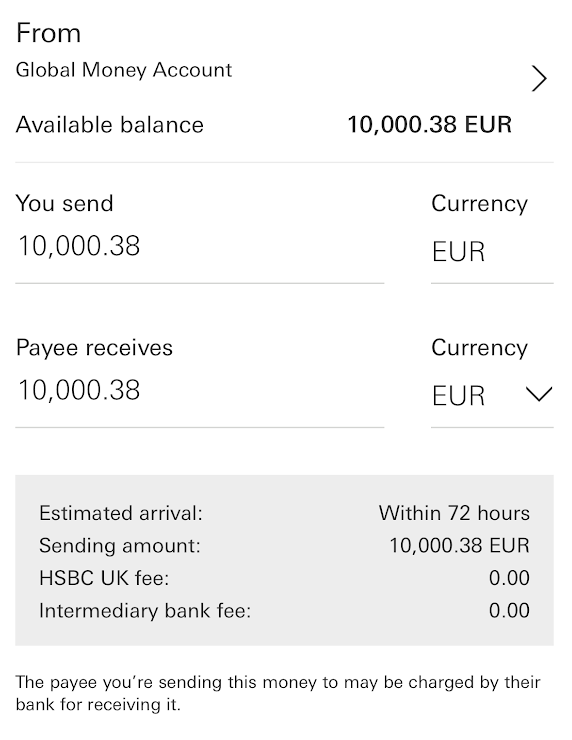

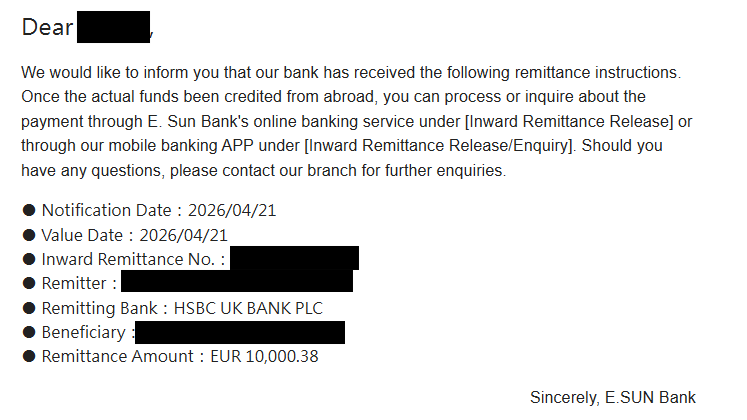

Today, I managed to transfer some EUR to E.SUN completely free of charge by using HSBC’s global money account: I loaded up my HSBC UK’s FCY account with some EUR (free SEPA transfer!). Then, I transferred this money into my HSBC UK’s Global Money account (note: the Global Money account can only be opened and used from the app - not from the website). From there, HSBC offers a free SWIFT transfer to Taiwan:

And more strangely: Unlike any other SWIFT transfer I had previously sent to E.SUN, this time they didn’t charge any fees. I fully expected to pay the usual NTD 200 (or so…) - but the app just showed “fees excluded” when releasing the money - and then no fee was charged!

So it’s actually cheaper and faster to send money from HSBC UK → E.SUN TW than HSBC TW → E.SUN TW

I just tried the process you illustrated and made a few tests, HSBC vs Esun vs Cathay today at the same time.

Sent to each of them USD 100 from my HSBC Expat account (where my Global Money account is), and it went incredibly well (HSBC ofc immediate with Global Transfer, Esun was credited this early morning, did the electronic declaration at 9am had to fiddle with their stupid codes which a few didn’t work, Cathay they called me and credited after 1 hr, dunno why didn’t receive the email/message to do online as it was the case some time ago). Neither Esun nor Cathay charged me any credit fee.

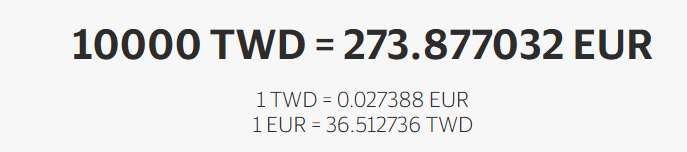

So, HSBC was quoting me 31.465, Esun 31.485 (special promo with the JX card), Cathay 31.48 (special promo with Eva card). Midrate is 31.52.

Hence, HSBC charges around 0.1745% conversion fee, Cathay 0.126%, Esun 0.111%. Will convert my money more from Esun now that I know this trick!

What’s the JX card? And how does the special promo work (any link to the promo website)? Will they automatically give you better rates just for having the card? Or any conditions / promo codes necessary?

I still don’t understand why that’s the case though

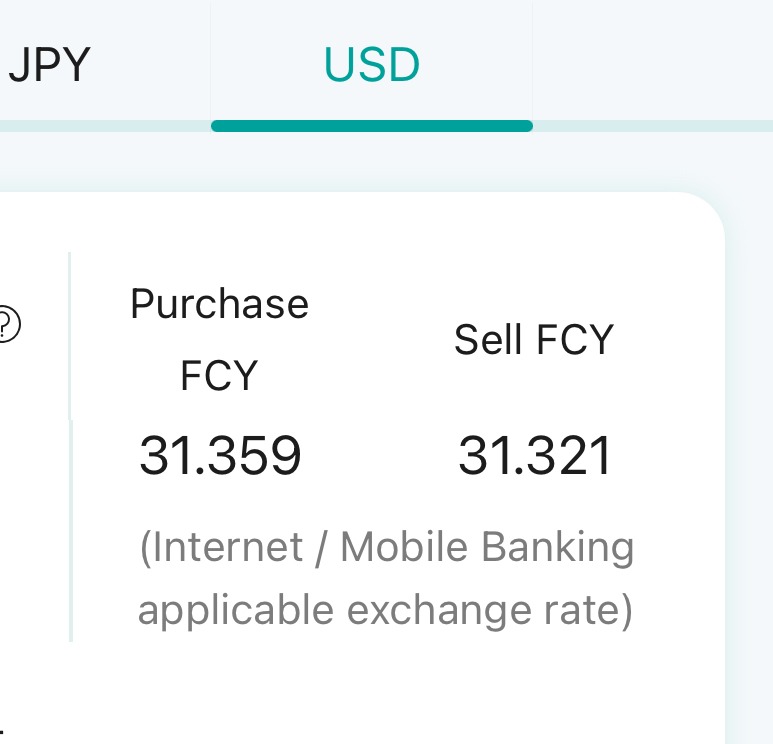

I currently don’t hold any Starlux card - for me, the exchange rates shown in the app are the following right now:

EUR Buy: 36.87 / EUR Sell 36.71 → 0.4% spread

USD Buy: 31.519 / USD Sell: 31.481 → 0.1% spread

Or are they cumulative?

(But that would mean that your spread becomes negative and you can purchase for less than you can sell…?)

FYI just sent a few thousands of USD to my cathay account to pay the credit card bill. Sent from HSBC expat at like 10 am, received the message to do the online declaration via app at midday, immediately credited, again no fee charged.