The Iran war thread I feel is not a place to discuss about energy or commodity shortages due to the Iran war coming up.

Taiwan is one of the most LNG dependant countries for energy worldwide, and LNG prices not only skyrocketed but there is bidding going on for basically every shipment now.

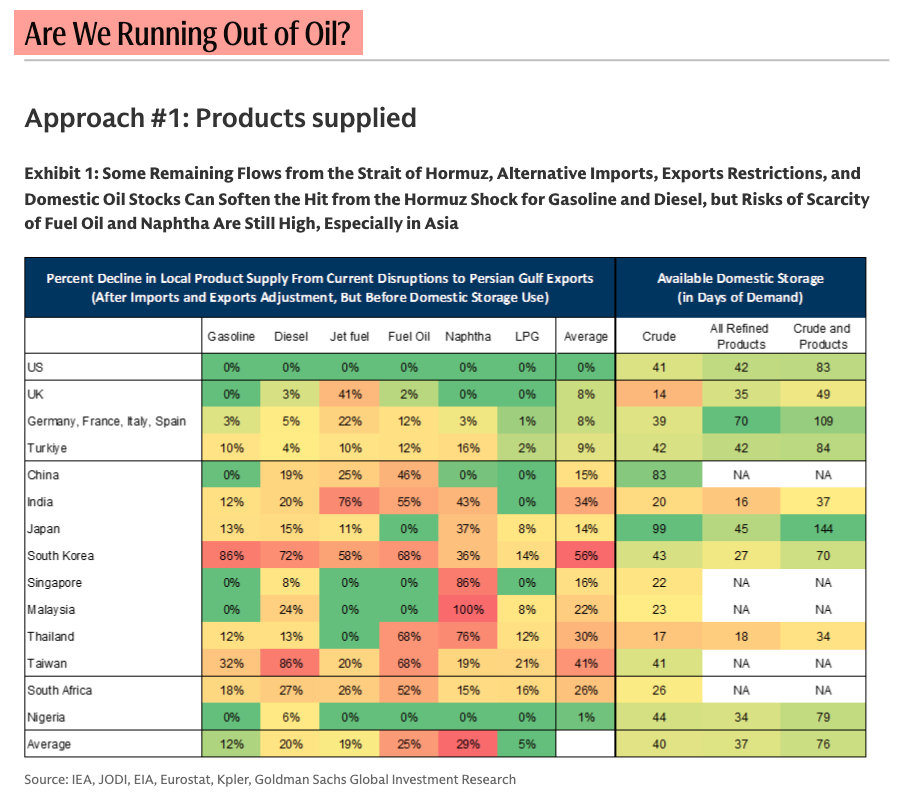

There is a shortage of around 20% of worldwide LNG but the rich countries seem to continue like always. While many poor countries shut down universities, schools and starting to shut down energy intensive industries like aluminium production, plastics production and fertilizer production the west carries on like nothing has changed burning through reserves in anticipation of Hormuz reopening very soon.

The problem here related to Taiwan isn’t so much the high value chip production, we all know they will be prioritised but the small manufacturers who operate on low margins. Think bicycle parts or car replacement parts (not OEM who are big)

Some interesting sources:

https://www.thinkchina.sg/politics/hormuz-closed-east-asias-energy-shock-and-strategic-shift

A summary of measures taken in a few south Asian countries: Iran War & Fuel Rationing – are “Energy Lockdowns” on the way? – OffGuardian

The UAE cut their oil production by half - so even if Hormuz opened up it will take at least a month to go back full volume: https://archive.md/F7TTH

The real problem for Taiwan however will arise when food gets scarce in other countries. Taiwan is not only dependent on LNG for energy, but imports a huge amount of food, and many countries will in a few months if this continues forbid food exports. India foremost but Thailand could join and that would mean rice increasing in price heavily. Again I don’t see Taiwan facing famine like many south Asian countries anytime soon, but it could mean cutting back heavily on meat and milk products.

Ultimately a cut back by 20% of energy must result in a similar cutback in consumption. And the more rich countries will price out poor countries the global problems get bigger. Ultimately supply chains are linked together. During COVID lockdowns there was a 20-25% cut in power usage worldwide. Lockdowns just a bit different could be needed again or pricing out of consumer groups.

I’ve found some comments that got deleted but I don’t know why about Taiwan listing out the awaited shipments. I’m not sure of the real source but to me it looks to detailed to be AI generated, I guess it’s a translation from Taiwans own energy ministry - it may have been retracted I don’t know why, because it looks pretty good vs the panic in poorer countries

Taiwan: Detailed timeline of the energy crisis

The structural starting point: why Taiwan is the most critical case in the developed world

Before getting into the calendar, it’s important to understand the combination of factors that make Taiwan a unique case:

The electrical mix at the moment of shock:

Liquefied natural gas accounts for approximately 50% of Taiwan’s electricity supply, and that percentage has been steadily increasing. Natural gas already powered 42% of the electricity in 2025, and the government aims to increase this to 50% by 2030. Simultaneously, the last nuclear reactor was shut down in mid-2025, and several coal-fired power plants have been decommissioned in recent years, so fuel substitution options are limited.

The actual reserve cushion:

Taiwan maintains energy reserves above the legal minimums: at least 90 days of oil, 11 days of natural gas, and 30 days of coal. Those 11 days of LNG are the key figure, because LNG is the marginal fuel that regulates half of its power generation.

The exposure to Qatar:

Qatar and the UAE contributed 8.4 million tons, 35% of Taiwan’s LNG imports in 2025. Global Scenario: Taiwan now receives one LNG carrier per day, compared to one every three days just a few years ago, and by 2030 it will need three every two days. The Startup Ecosystem: The logistics chain was already stretched to its limit before the lockdown.

TSMC’s special vulnerability:

TSMC accounts for approximately 10% of Taiwan’s total energy consumption. Energy-intensive manufacturing processes cannot easily reduce consumption without compromising production quality. A power outage of just seconds can ruin wafers in production.

The calendar: what has already happened, what is already inevitable, and what depends on variables

February 28 – March 2 | Week 0: The shock and the shipments in transit

The Strait of Hormuz was closed, and Ras Laffan was attacked. LNG shipments scheduled to arrive in Taiwan before March 15 had already set sail. Infobae reports that these ships—loaded before the closure—are the first and most important buffer. They are physical, they are on the water, and they arrive regardless of what the spot market does.

The government states that there will be no problems with LNG supplies in the first half of March because the shipments have already crossed the Strait of Hormuz. This statement is factually correct and not propaganda: those ships exist and are en route.

March 1-15 | Week 1-2: The last Qatari shipments arrive — a window of false security

The last Qatari cargoes loaded before the Strait closure are expected in Asia around mid-March. For Taiwan, this means that the system will absorb actual physical flow from Qatar until approximately March 13-15. During this period, the situation appears manageable.

What is already happening in parallel and is not visible:

CPC and Taipower are in the market desperately buying to replace volumes from April onwards.

Taiwan has secured 20 of the 22 LNG shipments needed for this month and next, with the remaining two still under negotiation.

The Ministry of Economy indicated on March 3 that units 1-4 of the Hsinta coal-fired power plant, totaling 2.1 GW, which were decommissioned between 2023 and 2025 and converted into emergency units, could be reactivated.

What is now inevitable at this stage: the price of gas that Taiwan is contracting for April onward is between 40% and 60% higher than pre-crisis contracts. That cost is already committed regardless of when the Strait of Hormuz reopens.

15 MAR — 31 MAR | Week 3-4: The first logistical gap — point of maximum initial tension

This is the most dangerous period of the immediate phase. The last Qatari shipments have already arrived or are arriving. The first replacement shipments—purchased on the Atlantic spot market or redirected from Australia/the US—have not yet arrived.

The logistical arithmetic is as follows: a shipment contracted in the Gulf of Mexico on March 1st takes approximately 35-38 days to reach Taiwan via the Panama Canal. That puts its arrival between April 5th and 8th. Any shipment contracted after the closure of the Strait of Hormuz will not arrive before the second week of April at the earliest.

Taipower has already begun stockpiling coal for the Hsinta nuclear power plant but acknowledges that restarting it remains a last resort. Hsinta units will only be dispatched when the operating reserve margin falls below 8%.

What happens to those 11-day LNG reserves? If the flow of arrivals is interrupted for 10-14 days due to the logistical gap, the storage tanks at the regasification terminals begin to drop toward the legal minimums. Taipower cannot allow them to fall to technical zero: there is an operational safety margin which, when reached, forces the activation of Hsinta.

What’s now inevitable this week: the possibility of a drop in LNG supply is forcing Taiwan to draw on its 13 GW of installed coal-fired capacity as backup. Although the government calls it a “last resort,” the physical logic of the system makes Hsinta’s activation in this window practically inevitable if the gap in arrivals lasts more than 8-10 days.

April 1-15 | Weeks 5-6: Arrival of the first replacement shipments — partial relief

Premier Cho Jung-tai announced on March 13 that Taiwan will increase imports of American LNG starting in June. This implicitly confirms that May is the most uncertain month: too late for Atlantic spot contracts initiated now, and too early for the new US flow beginning in June.

The first replacement shipments purchased on the spot market are beginning to arrive. The Ministry of Economic Affairs indicated on March 9 that Taiwan has secured 91% of its planned LNG arrivals for April. The remaining 9% is the gap that must be filled with coal or by drawing on reserves.

What the 91% hedging figure for April doesn’t tell you: it covers volume, but not price. Exposure to the Taiwan spot market already exceeds 30% of its imports, and any additional purchases during this period of extreme volatility will significantly increase costs for CPC and Taipower.

Industrial restrictions in this phase: Although there are no residential outages, pressure on the grid’s operating reserve margin is forcing Taipower to activate industrial reduction protocols. Large industrial consumers—steel mills, petrochemical plants, cement plants—are the first to receive requests for voluntary reductions or scheduled outages. TSMC, as an ultra-high-voltage customer with special status in Taipower’s regulatory protocol, maintains priority supply but at prices that are skyrocketing.

April 15 – May 31 | Weeks 7-13: The period of greatest accumulated vulnerability

This is the most structurally challenging section. Several factors converge:

1. May: the month without confirmed coverage

Authorities have secured LNG supplies for March and April, while seeking alternative sources for May. The fact that they are still “searching” for May in March 2026 confirms that coverage for that month is uncertain. The contracted Atlantic shipments are now arriving in April-May, but competition with Japan, Korea, and Europe for those same shipments is fierce.

2. The lag effect of oil-indexed contracts

Most LNG contracts are indexed to the price of oil with a three-month lag, meaning that import costs for Asian buyers will increase from June 2026. This adds a second wave of financial pressure just as the system begins to physically stabilize.

3. Summer and the demand for cooling

Taiwan experiences hot and humid summers. Electricity demand in the summer is up to 15% higher than the annual average. China could exert hypothetical pressure on the grid when it is most vulnerable, that is, when there is less supply and more demand: in the summer. Although this refers to a different scenario, the physical risk is the same: the operating reserve margin in July-August could fall to alert levels even without further interruptions.

4. Wood Mackenzie quantifies the damage

If the disruption lasts two months, regional LNG demand in Northeast Asia could fall by 4 to 5 million tons in the third quarter of 2026. For Taiwan, some of that demand destruction is involuntary (the gas doesn’t arrive) and some is forced (coal is consumed instead).

JUN 2026 onwards: The new balance — more expensive, dirtier, more fragile

Taiwan signed a purchase agreement for US LNG with Cheniere Energy on February 10, with deliveries beginning in June and annual purchases of up to 1.2 million tons starting next year. This flow begins to arrive in June, confirming that before that date the system operates in permanent emergency mode.