I am having a hard time with this, but unfortunately there is a loophole here.

CRS and tax withholding have 2 separate standards here, so there is asymmetry.

Banks are required to withhold the tax on interest when the interest is paid, or incur in immediate fines.

This matter is not regulated by the FSC, but by the Tax Bureau and so refer first to the Income Tax Act and in particular to Standards of Withholding Rates for Various Incomes by the Ministry of Finance.

Art. 7 of the Income Tax Act is where tax residency is defined, and unfortunately the way how it is worded and with the other features of the legal system of TW, only Nationals with Household registration are assumed to “…ha(ve) domicile within the territory of the Republic of China and resides at all times within the territory of the Republic of China;” (I know that domicile (住所) does not equal household registration (戶籍), and there are even Supreme Court rulings on this, but banks here act with a principle of prudence and conservatively, and they actually legally can do this…)

All other persons, NWHOR, foreigners with ARC, foreigners with APRC, non-residents, are assumed not to be tax residents of TW unless they can prove otherwise. Unfortunately for this the burden of proof is on the client.

The proof for tax residency with the Tax bureau comes usually during the tax declaration each May, where we indeed declare how many days we stayed in TW, which then the Bureau checks with NIA thanks to the Entry and Exit certificates and logs and confirms it, applying thence the relevant resident tax rates according to the income declared. This tax rates is then retroactively applied to the interest paid and withheld by banks with “tax credits” towards to tax payable amount.

This is the conundrum: banks can’t afford to withhold the wrong amount, so they always assume foreigners not to be resident and withhold the max (20%), unless the foreigner proves to be tax resident somehow during the year (like with an entry and exit log), which then will withhold the resident rate (10%) for the remainder of the year. Hence they also need to modify the CRS declaration to be consistent, since CRS for them is the lesser pain to make “wrong”, they don’t get fines there immediately.

There is no solution until a legislative modification is made, since there are asymmetries in the declaratory periods and withholding periods, and also no easy way for various agencies and industry participants to communicate and share information.

This is also the reason why many employers, if they withhold taxes directly from the payslip, for foreigners just withhold for the first 6 months the non resident rate and then they “adjust”, or they get fines and just choose the lesser pain, i.e. inconvenience for the foreigner, understandably.

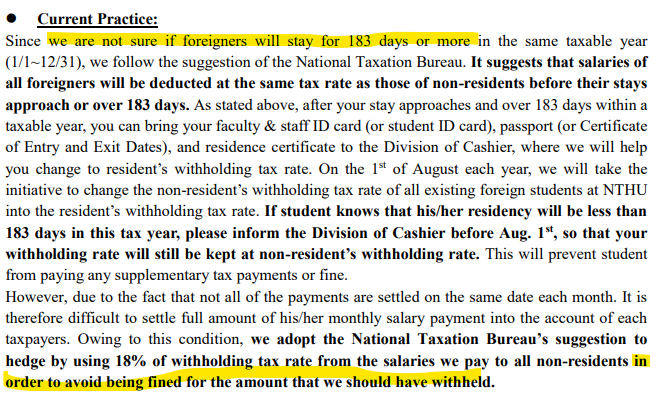

Below a excerpt from the National Tsinghua University brief upon recommendation of the Tax Bureau:

This is a battle we can’t win with the current rules, I am defeated, I concede. Rules have to be changed, but require a quite deep revamping of the system.