It doesn’t. There is a company that will help you buy an actual property that they find in a solid area…for renting…and get you a company to run the day to day. THEN those costs would come into play.

Yes in Taiwan. In the States and Canada property maintenance and house insurance is becoming so high that it doesn’t make sense to buy a property as investment unless you’re living in it. In comparison the guard fees and earthquake insurance won’t break the bank, and shouldn’t discourage buyers from investing.

And if you rent out property it can be damaged and the cost to fix it exceeds the rental income, suing the tenant takes time, energy and money. In the end your gain is nil!

Well at the very least, this thread shows me I am not alone in how I feel about real estate.

Renter’s insurance.

I’m not about to get into a discussion about the relative merits of buying real estate, but I will say I made a lot of money off real estate a couple years ago so there’s that.

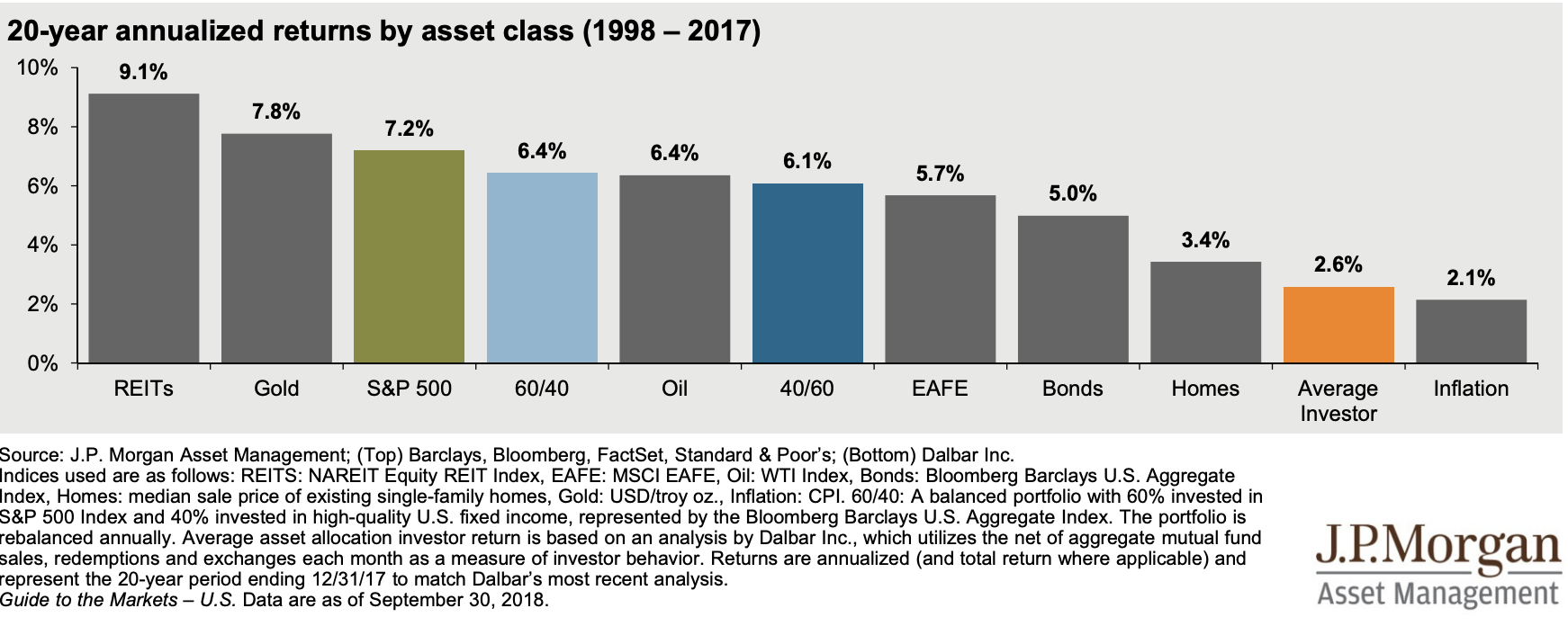

JP Morgan recently compared the performance of different asset classes - over a 20 year period. Home ownership is quite poor - I guess they didn’t include ‘rental yield’ - perhaps they should have because over the very long term that’s all you get - the value of the home eventually depreciates to zero.

Remember REIT dividends are taxed as ordinary income, so that 9.1% is slightly misleading unless held in tax-advantaged accounts. They do, however, starting from last year, benefit from the 20% deduction allowed for pass-through entities, which makes a compelling case for increasing allocation in REITs even in taxable accounts moving forward.

An REIT fund (VGSLX, for example) is a reasonably safe option to increase exposure to real estate without having to deal with the hassles and risk of actual property ownership.

Just for comparison sake in the west.

5 acrea residebtial la d eest coast canada rural with 2 houses costs ys 2500cdn for property tax. Insurance can vary a lot. If the owner lives there majority of the year 900/yr. We rent one out so 1800/yr and empty would be around 3k. But they look at a lot of things like eletrical panel, water source, foundation etc etc.

All tolled with city water being high 3900 cdn yr. About 90 to 100k nt depending on exchange rates.

I can run my business through it.

Rent out one house cheap to a family member at 600/month (easy to get 1k in sw canada but with family i have literally no problems) . so 7200/yr and half goes to gov. Other house could be rented easy enougb but i am using it. So easily 20k a year. Rental agency qupted me 130/month to manage it but things go down hill fast with those guys.

Houses costs 250k 10 years ago had offera up to 440k recently. Can make more money probably in 10 years if you are money smart. But this is easy and provides me with a priceless sense of security and makes it easy to push forward with other ventures. Im of the mind its always good to own land (debt free) and go from there.

Thanks a lot for sharing. I don’t deny the feeling of security, I am just not sure how real it is. Especially on the East Coast - where are you exactly? I have friends on the East Coast ( rural Nova Scotia ) who state that although the value of their place has increased since they bought it ten years ago, they are having a very hard time selling their place. This echoes what many have said for most of Nova Scotia’s real estate market, and thus why some retirees move out East to retire if they want to stay in Canada.

If you feel comfortable with it, I would like to see a transparent statement of your expenses (including interest and mortgage payments, property tax, insurance, repairs, etc.) vs income generated - your post wasn’t all that clear in expenses vs income and actual profit.

Another question, do you have any investments outside of your property? Or is all of your net worth wrapped up in just your property? And in truth, your situation is kind of different - you have blended a residential and commercial property ( I don’t want to even imagine your taxes!).

My original post was about people who only have their house (often an expensive one) and pump all of their money into their house as their sole investment.

I kind of see this mentality as left over thinking from the time of defined benefit pensions - if your pension is taken care of, then all you need to do is pay off your house and you are golden for your retirement. Good defined benefit pensions are rare beasts these days, but the paying off your mortgage as THE great (only?) investment continues to be seen by some as the best method to financial success - I am just not convinced it is the case.

Excuse the typing above. Bad even for me. Came west today and its rainy and humid so my phone is acting up again. Im near the coast now, drier should be back to my normal big finger typo style.

for everyone it will no doubt be different.

In my opinion central and east are not as good. I am on west coast. Seems more is going on there. Much of canada has the issue of lack of work, hence cheap real estate. Where it is booming its not cheap. And then there are variable areas that are hit and miss (oil, mining etc towns) The east is also cold as shit so not my cup of tea. But thats the great thing is that different people lime different things. I like humid rainforests and big trees. Many find it damp and depressing. So it is hard to put a value on that as people value different things. Probably explains Alberta and the folks that live there…![]()

I like west coast due to business ease wit Asia, which will only get stronger. Logistics.

Here is a more organized list of my expenses. It will change for everyone.

My land 5 acreas with 2 houses.

Residential zoning and not in a municipality or city so its regional district. This means run by the provincial goverment for purposes of easy conversation.

Allowed to run a business, without a business license on this type of zoning (thats why i chose this area!). So taxes are WAY lower than commercial land. That said im in the bio sector not things like machines, computers, plastics etc etc so its possible to run the land for business this way. Even processing and manufacture just need to read the laws. Same goes everywhere. Anyway its not the point so i will leave out my business aspect and treat it as a 2 house rental property for numbers sake as if i was renting it out.

My costs now as follow (rounded numbers)

All in cdn per year

Property tax $2,500

Insurance $1,800 (as a rental, 900 if i lived there)

Second house add 1600 if rented.

Water bill $800 ($200/3 months, wierd situation making it crazy expensive, gov privitized it)

I did all the work to fix them up. Spent about 20,000 for both houses and they were in bad shape. But thats just luck that we can do the work ourselves. Probably closer to 80,000 if we hired others to do everything. Ontop of 250,000 purchase price.

4 acres are forest so we can forget that part. 1 acre is landscaped and lawn. We did it. If we are here we can pay someone $80 twice a month to mow and trim grass. $1,440. I rent to family cheap so they take care of it.

As its all fixed there is relatively low maintenance fees.

Big things i view are

Roof $3000 material/20 years $150/year x 2 houses, 300

Appliances -stove, fridge, dish washer, laundry set- lets say (guessing) 2000/10 years so 200/year x2 400

Repaint, floors etc (we export wood floor so luckily quite easy for us) but say avergaes out to 100/year x2 100

Probably other minor stuff but im rounding up as we always should.

So i get $9,040cdn/year roughly.

House cost 250,000

Fix up 80,000 if contracted out(people can easily cut that down by working but if you get paid well why not hire someone cheaper than yourself?)

Total $330,000cdn (my cost was only 270,000 due to renovating ourselves)

Income generated

Average rates for my area are about 1100 for the bigger house and 850 for the smaller one. I only rent out 1 for 600 to family cause they need it and i hate headaches!

Bit leta low ball and say 700 and 900 for the 2 houses. In the 8ish years ive owned them, never sat empty for more than a couple weeks (another advantage of western canada). So lets say 1 month a year not rented out. 1600x 11months is

$17,600/year

The land we also get constant inquiries to rent put as farm land. Mostly organic farmers and landscape/nursery type businesses. The cheapeat offer was 1,800/year per acre. I qont cut the tree so only have 1 and a bit. So plus 1800/year pretty easy if i wasnt using it myself already.

$19,400/year fairly easily.

-$9,040 costs

= call it 10k.

Minus income tax based on your bracket.

Big money? Nope. But still money. And i can use the property to get loans for other business easily, makes tough times slightly more stable etc etc.

I paid in cash as i had worked my ass off in taiwan for 10 years saving every scrap of change i could. So mortgage is a variable.

The land has gone up over 100k so lets round down and call it 20kyyear until now. That cant really be calculated long term but can if flipping it. Subdividing gets me 140k per acre lowball in the area with just land, driveway and perk. So 15k costs and tax probably still 90k profit and could divide into 3 lots, 2 with houses so even more. Etc.

Do i do this to make money? No. But it is sustainable and provides a stable base. Especially nice when overseas. In the emd the area is easy to sell and likely alwaya will be as long and the country doesnt tank.

For taiwan…totally different game. East coast has problems just like the rest of the country. The advantage there is taiwan health and environment is so dire there is a small migration happening with middle aged to retired people who are trying to find a healthier retirement lifestyle. I dont seenit getting cheaper there. I have bought land here before and its 4x what it was 7 years ago looking at what neighbors are selling it for. But with government stepping up law and all that it seems like a losing game here now. I wouldnt buy anymore unless i wanted my own nice house that i can live in. But thats kust a want, not a business decision. I pay 6000 rent here now. My whole time in taiwan i have paid between 2000 and 7500. Mk th rent for a house…houses before could be had for a million easy, court sales are interesting. Now its triple plus (south).

At 7000 rent minus other costs it only makes sense if speculating and flipping. Keep it lived in via renting. Taiwan houses tend to have far less repair issues though due to concrete vs wood frame and not picky vs princesses.

Thanks for the clear and honest answer. It isn’t that I hate real estate, not at all. I just have quite a few friends and family that only have their house, and that is it.

My mother-in-law is so bad that she has only her government pension (CPP and OAS adding up to maybe $1500 Canadian per month) for her retirement income. However, she is sitting on her house that is worth $300K, that is paid off and she won’t sell it or consider a reverse mortgage or use the equity in any way. Her situation isn’t really all that unique either.

Yes i agree. But that isnt smuch a cult of home ownership. That is more the cult of not being hungry. LOTS of people just want “good enough” and carry on as is. I find it is often the same type of person that thinks you have to go to university. Just cause you were told it was a part of the process.

Not much thought and especially not much effort goes into pushing harder. But its ll part of the economy. We need those that innovate and we need those that work in the factory. The nice part is we all have that choice whether we want to admit it or not

I agree with others that buying may not make sense in areas, like Taipei, where rents are very low compared to mortgages. But to me the situation is different if the mortgage payment (with standard down payment) would be similar to rental costs and the market is not at a sharp peak. Regarding leverage, you turned a $3k investment into $30k while probably breaking even or having lower monthly payments than you would renting, and with very little risk. Not bad! AND, the mortgage won’t change, aside from insurance and taxes, until you pay it off. While rents will keep increasing. So if you see yourself staying in a place for a long time, and the market is not at a peak, there can be a lot of advantages to buying. I have been fortunate to be in a strong housing market in the US for nealy 20 years. If we were to sell our home today, the return on our initial downpayment would be far greater that the returns we have made on our index fund investments over that time, because of appreciation, paying down the mortgage, tax incentives, and using home equity to finance college tuition and a rental home purchase (which has also appreciated).

Prices in Taoyuan are ok, like you said if one knew they would permanently live there it would be fine to purchase in Taoyuan or an area where the building you live in has rent comparable to a 30 year Mortgage after 20% down. Taipei prices are still insane, New Taipei City insane.

US may have some opportunities after this virus plays out depending on which city. Also I think Malaysia specifically Kuala Lumpur is a decent time to buy the next few years for many reasons.

You know if the government wants to deal with the problem of a large number of house sitting empty, they could tax empty houses at a horrendous rate, but give serious exemptions if the owner rents them out (like massive tax cuts, zero tax, etc. to encourage the landlord to reduce rent).

There are lots of house in Taipei but most of them sits empty because the landlord won’t rent them out! If they get encouraged to rent them out then maybe they will.

Good exchange rate in Malaysia right now, too! I have been looking for an opportunity to move there or Taipei, but I like Taipei much more. Maybe because I lived there but only visited KL. Are there reasons other than the exchange rate that make it a good time to buy in KL now?

It seems to be a bit of a sellers market in our corner of the US right now–combimation of low mortgage rates and low inventory because people don’t want to show their homes.

@jeff In relation to the main topic, I agree and disagree at the same time. Ultimately, you need a place to live, so if the cost is about the same, it probably makes sense to own, especially if you are staying in one place for a while.

However, even looking at my situation, it is not as simple as it seems - as a homeowner I have multiple expenses that I would not have as a renter.

Let’s look at it as a whole:

-

Mortgage payments : $500 equity ( gain)

-

$500 interest (loss)

-

House insurance: $150 (loss)

-

Property tax: $200 (loss)

-

Home maintenance : $300+ (loss)

The above does not really take into consideration any larger repairs ( furnace, roof, foundation) that tend.to happen every decade or so with owning a house.

Looking at it, it is a net loss of $650 per month. However, you do need a place to live, and if you consider a place to rent (average) of $1000 / month, and the cost of my house is $1650 a month, with a $500 gain in equity per month, the expenses come out to being $150/ month more with my house. Not a huge amount, but compared with a 5% per year return in an index fund (considering inflation to be same for both), for a monthly contribution of $150, it amounts to a loss of $90000 over a 25 year period. Not peanuts to be sure.

I personally find that utility expenses are much higher in houses versus apartments as well. Add on top of it that it is likely that most people’s mortgages are much larger, with more interest to pay over a 25 year period, and it still doesn’t make sense to me. But, that is just me. Everyone is different.

@Noel. Good points, and buying is of course not always the right choice even where I live. That said, we do get a tax break for the interest and property tax (though much less with the last tax “reform”). And it is also nice that the ratio of principle to interest increases over the years. Ten years into our current mortgage, our total expenses including tax and insurance are about 20% less than we would pay to rent the same house. That leaves quite a bit for unexpected maintenance.

Interesting - Canada is a bit different, we cannot claim the interest on our house loan, and our property tax is only claimable in a very limited manner.

Still, I am not against the idea of owning property in some circumstances, for sure. I just have friends with $800,000+ houses with no investments at all, and I just don’t get it.