I had a previous 24 month contract for my phone that I accidentally bailed on due to covid and being stuck in the US and now I’m afraid to return to that store or they may ask me to pay up the ~5 months of bills plus late fees. Can a different store find out about it? What happens if they send it to collections - will the first store report it against my ARC number and is it there any credit score tied to it? What about credit cards - do they look at your current earnings or previous history on the ARC number?

In the US pretty much everything is tied to your SSN. Is it the same in Taiwan? I know in India it’s not because their country has hundreds of different social identifier codes.

Yes credit cards and loans do give you a credit score at the JCIC and it is tied to your ARC.

Phone contracts do not afaik. However skipping out gives justification for phone companies to require guarantors and deposits from all foreigners as they can claim incorrectly that all foreigners leave without paying.

Personally I’d go pay them back before trying to get a new line with all the buhaoyisis you can muster. (Not saying you intentionally didn’t pay, I get the covid reasoning)

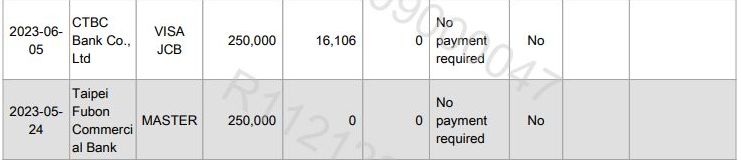

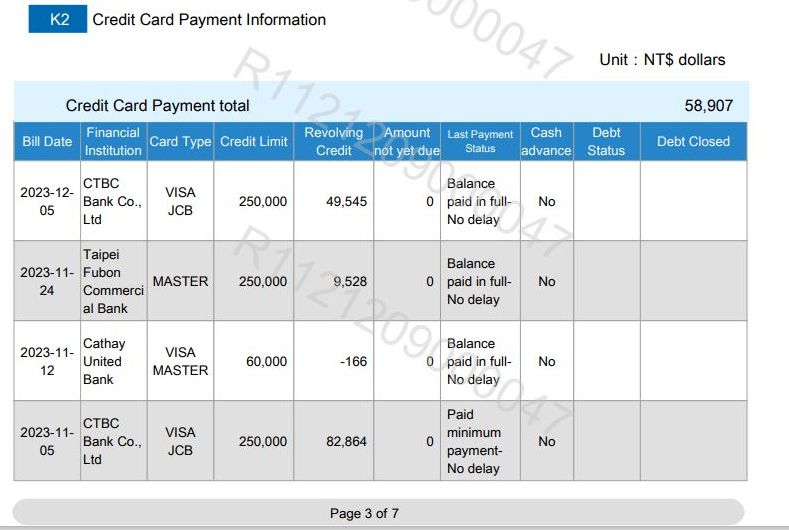

I just checked mine. I have 4 credit cards… three have NT$250k limit and one card NT$60k limit. Total credit limit NT$810k

My credit report shows all cards are paid in full each month. For one month with my CTBC card I paid maybe 50% of the balance but the credit check simply says paid minimum payment no delay. I have no late loan repayments as no current loans. Have no cash advances or other debt.

for my CTBC card for last six months I have spent and paid NT$461k… My Cathay Cube card has had a credit surplus of NT$166 as not used since Fubon took over from Coscto. Before I got my CTBC China Airlines card and the Fubon Card all my credit card use was on the Cathay Coscto card… 60K limit but would run it down to owing 55k, add 60K and a couple weeks later do same again. Did that for years lol.

My Fubon card since September to now has a spend of NT$132K Just paid my card off in full yesterday. So may average monthly spend is just under 100K on my credit cards and they are paid off in full every month.

Yet I get calls from financial institutions asking would I like a loan every week.

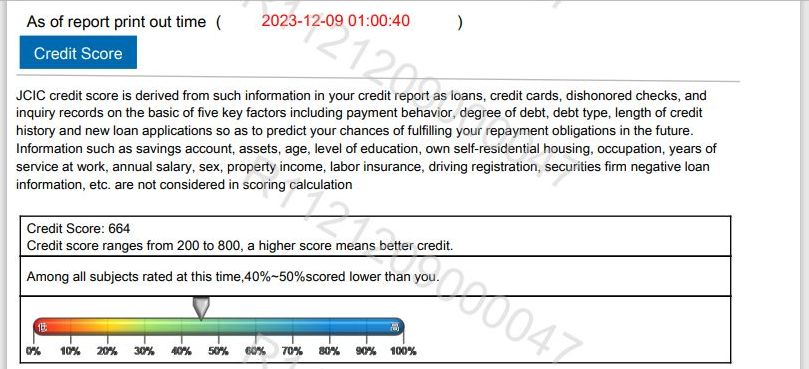

My credit score… 664 lolz I think I’ve been cheated.

I have been doing mine once a year for last couple years. Last time was a few months ago, I was just a few points off 800. That’s with 2 credit cards and never having a late payment, always paying in full.

If you have been paying them off on time and in full, only explanation for your low score is your high usage. Not sure about Taiwan, but in other countries using almost all of your limit is not good for your score.

I go get the paper one each time I apply for a credit card because online doesn’t seem to work for me. Can log in, generate the report, but then it fails the decryption step for some reason.

Never been close to my limit on my cards with 250K. High usage should never be a concern when cards are paid off in full. After all what are credit cards for if not for being used lol.

100k a month between mainly 2 cards is high usage? lol The two cards I use have 250K limits and rarely get above 50k used and only one time on one card 100k paid off in full.

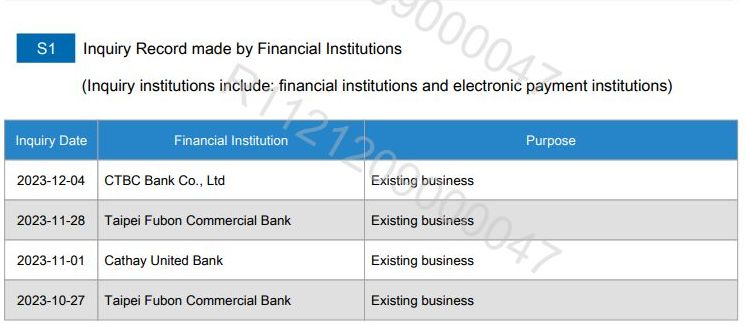

I see Fubon Cathay and CTBC run credit checks again in late November and early December… so not like they do not have my spending and payment records. Let’s see in another 6 months.

One thing my record shows my Fubon card as being issued since May which is impossible as I didn’t apply for it until August lol Also if such a bad credit risk why would Fubon issue a card with a 250K limit. No financial documents were submitted to Fubon. So they did check my credit history in May 2023 as well I assume preparing for the handover from Cathay.

5 major factors that deduct points from your credit score

The credit transaction time is short or the information is insufficient: there is no valid credit card that has been held for more than 3 months, the credit card payable amount in the past 12 months is not greater than 0, there is currently no credit information for 3 consecutive periods, and the credit balance of the past 12 periods None are greater than 0, etc.

Various unpaid records: personal credit, mortgage, car loan, credit card, etc. The number and frequency of late payments will affect the score.

Credit card usage status: length of time the credit card has been held and whether the payment usage record is normal

The degree of personal credit expansion: including the total debt, the generation of cyclic interest due to paying only the minimum due on the credit card, using the cash advance function of the credit card and other cash cards, applying for unsecured loans and initiating cyclic interest, all of which represent low repayment ability. , the score will also be lower

Number of joint inquiries: If the number of inquiries exceeds 3 times within 3 months, it means that you will only apply if you have urgent financial needs, so the lower the score.

This is one that I know trips people up, having multiple credit cards can lower your score even if you seldom use them.

A friend of mine was told by the bank to reduce the amount of cards he had when he was applying for a mortgage, as having so much open credit was increasing his risk.

I can’t remember if it was 3 or 4, the advice was to just stick to one and don’t apply for credit you don’t need. It worked as he got the mortgage at the rate he wanted, but I don’t know all the in’s and out’s. I think he had applied for them over the years because of better rates and thought he was improving his credit history so never cancelled them.