after wiring money to my Taiwanese bank account a couple of times in the past, I was getting tired of needing to visit the Bank (E.Sun) every time I made a transfer. Somehow I managed to set up the “online remittance” feature by filling out another form during my last visit. Now I’m trying to use this feature for the first time…

Previously, I would just tell the bank employee in the branch that the money came from my savings account in my home country and I was using it to pay for expenses here in Taiwan. And they were happy with that and released the money (after me signing some form in Chinese).

However, using the online remittance, the bank is asking me to declare the nature of the transfer using some predefined codes and I am not sure which code to choose.

From what I understand, It seems that they want me to declare the original source of the money (so I can’t just choose something like “living expenses”).

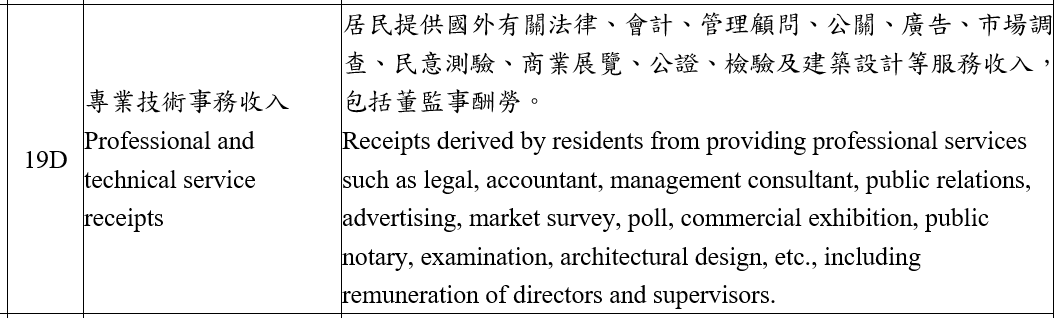

However, the banking interface does not allow me to select code “410: Inward remittance of residents’ wages and salaries” (because technically the money I sent mostly consits of my salary for remote work performed in Taiwan). I could select “19D: Professional and technical service receipts” - but I am not sure if that’s the right code in my situation or not…

Mhh - that would be quite far from the truth unfortunately.

Is there any reason behind this?

Why can citizens receive “wages and salaries [from] foreign companies without business registration in the R.O.C.”, but non-citizens can not?

How about 399:

399 其他外國資金之流入

Other inflows of foreign funds 上述各項以外之外國資金流入,請詳述性質,如押標金、保證金(不含衍生金融商品及借券交易之保證金)等。

Inflows of foreign funds other than those described above (please specify the source (residents)/ purpose (non-residents)), such as bid bonds or performance bonds (excluding margins or cash collaterals for financial derivatives or securities borrowing).

Quick update to that one: Today I went to E.Sun again and the employee handling my incoming transfer told me again that I can just do it online.

They told me I just just use code 510 because it would be appropriate for me if I send money from my own account to pay for my living expenses. Probably that code causes the least amount of paperwork for everyone involved

To send money to my own-named bank account back home for whatever purposes, I have always used 510 for years and years through my online banking (a competitor of E.Sun) as per advisement from a counterperson at my branch.

Right for what? From the list of occupations, that reads to me like it’s referring to professional practice income, which has a specific meaning.

Even if that’s what @qwert_zuiop does for work (and I think it might not be, though I could be wrong), I don’t think this category would apply to someone transferring money already paid overseas to their own bank account in Taiwan.

…right for OP’s user case, in fact he already mentions it in the first post but that is left inconclusive.

Perhaps someone with banking insights (@Mataiou ?) could comment about the chain of bank accounts through which professional fee payments arrive. However, as I understand the tax burden should be carried where the service is rendered, if the money ends up in Taiwan, this is a transparent way to make that clear.

I’d be happy to hear of actual experiences with this, though…

OK, in a generic way:

European client pays a fee for professional consultancy in to an account in Europe. The consultant then transfers it to an account in Taiwan. The discussion is about which “Remittance code” is correct to declare for the bank here.

This isn’t what determines the tax burden though, AFAIK. At the time of transfer, the money is now just money in an overseas personal bank account being transferred to a Taiwanese personal bank account — I find it difficult to see how money in a bank account forever retains the property of how it was derived, i.e., in this case being professional practice income (tax code 9A, defined in Article 14 of the Income Tax Act).

What happens when there’s other money in that bank account? Let’s say someone had US$100k in an overseas bank account (savings etc., all derived from somewhere and some activity) then received US$5k in what Taiwan would consider professional practice income from an overseas client.

They then transfer US$5k from that account to their account in Taiwan for general living expenses. Or US$3k, or US$10k. Is that still professional practice income, or is it now just savings the person is transferring to themselves? What happens if they leave the money for now but transfer US$5k two years later?

In any case, my main point there was that 19D does seem to be talking about professional practice income (or something quite close to it), and I’m not sure that’s what @qwert_zuiop is doing. (Even if it is, I think it’s not what most of us are doing.)

I should add that I’m not sure what the correct code is either. I looked through the list twice and nothing stood out to me as clearly the right choice.

The closest I could get was “Errr… maybe that one would be okay?”